Most American homebuyers will pay more in interest than they paid for their home. On a $400,000 purchase at today's rates, a conventional 30-year mortgage costs over $430,000 in total interest alone. A halal mortgage eliminates that entirely — and it is available in 27+ US states right now, to anyone regardless of religion.

This guide explains exactly what a halal mortgage is, how it works step by step, what it actually costs compared to a conventional mortgage, and how to apply for one in the United States.

What Is a Halal Mortgage?

A halal mortgage is a home financing arrangement in which the bank and the buyer jointly own the property together, with the buyer gradually purchasing the bank's share over time. Instead of charging interest on a loan, the bank earns a return through rent on its ownership stake. No interest is charged at any point — the bank earns profit through co-ownership and a fair rental arrangement, not through debt.

The term "halal" means permissible under Islamic law. But halal mortgages are not exclusively for Muslims — approximately 23% of halal mortgage customers in the United States are non-Muslim. They choose these products because the structure is genuinely fairer: the lender shares ownership of the property, which means they share the risk. That is fundamentally different from a conventional mortgage, where the bank profits regardless of what happens to you.

How Does a Halal Mortgage Work? (Step by Step)

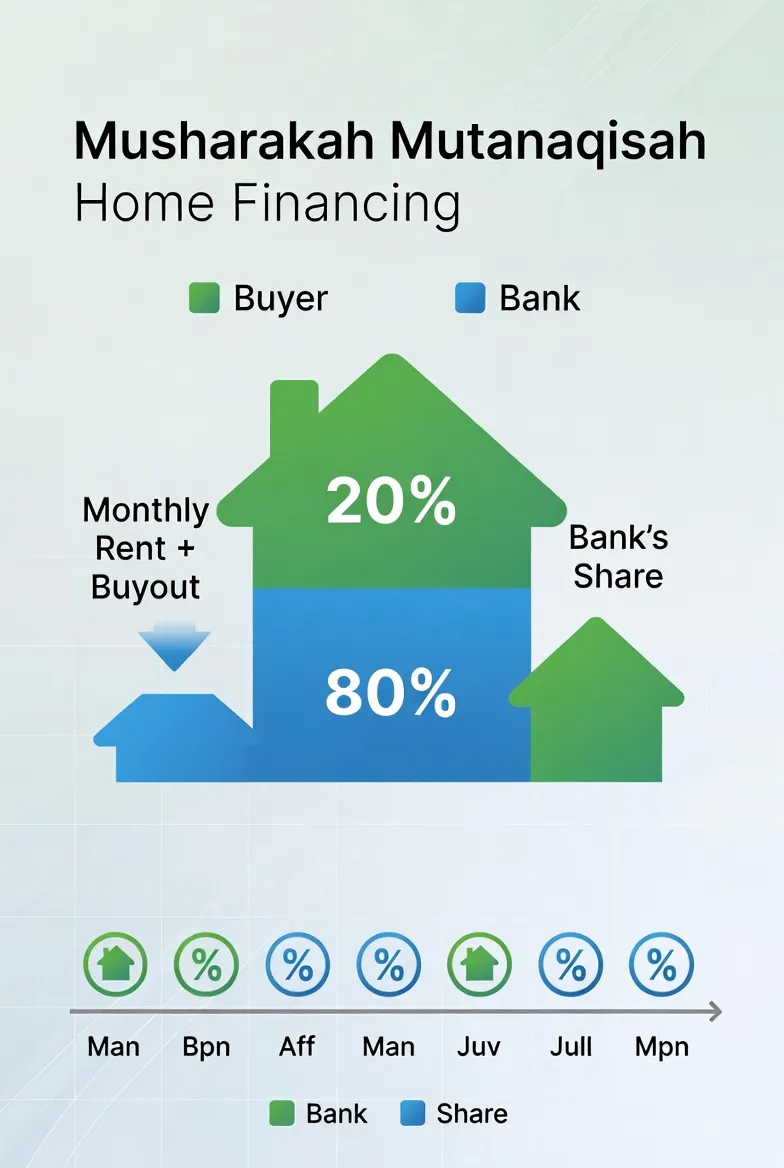

The most common halal mortgage structure in the US is called Musharakah Mutanaqisah — diminishing co-ownership.

Example: You want to buy a $400,000 home. You have $80,000 saved (20% down payment).

Step 1 — Joint Purchase

You and the Islamic finance company jointly purchase the home. You contribute your $80,000, giving you a 20% ownership stake from day one. The finance company contributes $320,000, giving them 80%.

Step 2 — The Lease Begins

You want to live in the home. Since you only own 20% of it, you pay rent to the finance company on their 80% share. This rental amount is calculated based on a fair market rate benchmarked to SOFR (the Secured Overnight Financing Rate).

Step 3 — Monthly Buyout

Each month, alongside the rent, you purchase an additional unit of the finance company's ownership stake. As you buy out more of their share, the portion of the property you are renting decreases, and so does your monthly payment.

Step 4 — Full Ownership

After your agreed term, typically 15 to 30 years, you have purchased 100% of the finance company's stake. The deed transfers fully to you. You own the home outright, having never paid a single dollar of interest.

The Critical Distinction: In a conventional mortgage, you are a debtor. The bank owns your debt. In a halal mortgage, you are a co-owner. The bank owns a share of the property, not a claim on your future income.

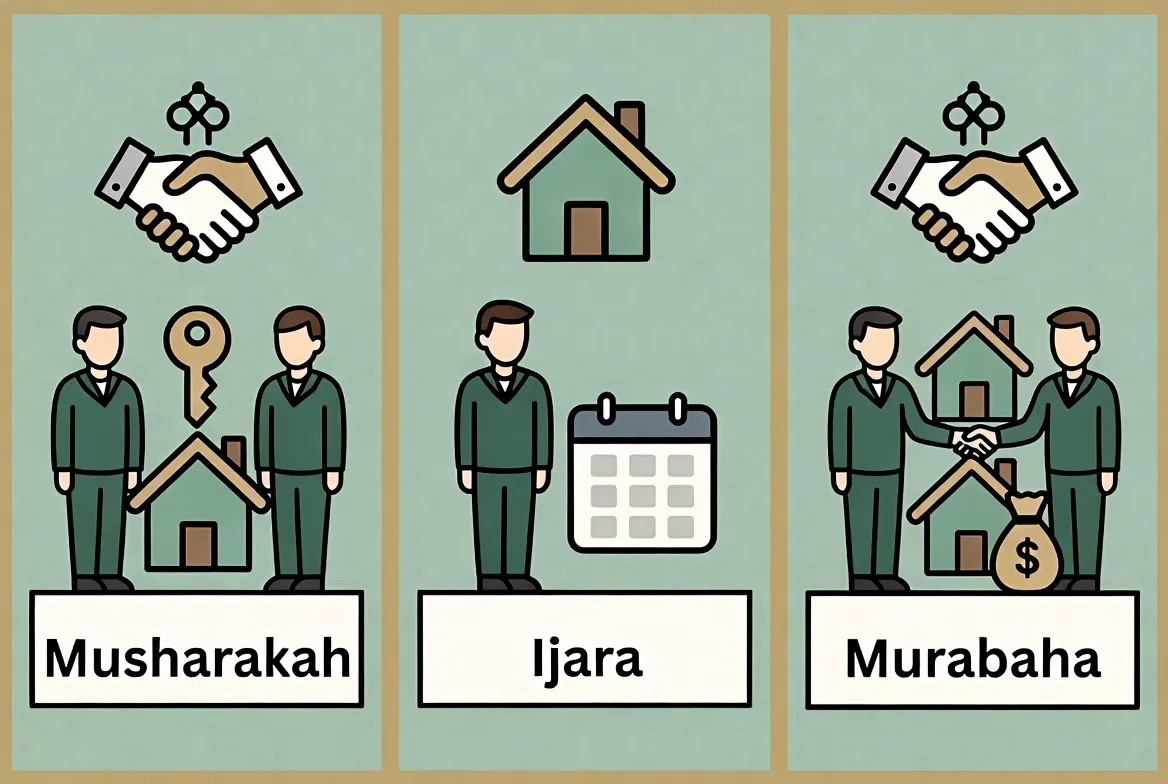

The 3 Types of Halal Mortgages Available in the US

Three Sharia-compliant home financing structures are available to US buyers in 2026.

1. Musharakah (Co-Ownership)

Bank and buyer co-own the home. The buyer pays rent on the bank's share and gradually buys it out over time.

Best For: Most buyers and long-term homeowners.

2. Ijara (Lease-to-Own)

The finance company buys the home and leases it to you. Ownership transfers to you at the end of the term.

Best For: Buyers who prefer predictable fixed payments.

3. Murabaha (Cost-Plus Sale)

The finance company purchases the home and sells it to you at a disclosed markup, payable in installments.

Best For: Shorter financing terms and specific purchase situations.

For most US buyers, Musharakah is the recommended structure because payments decrease over time and the co-ownership model most clearly reflects the risk-sharing principle at the heart of Islamic finance.

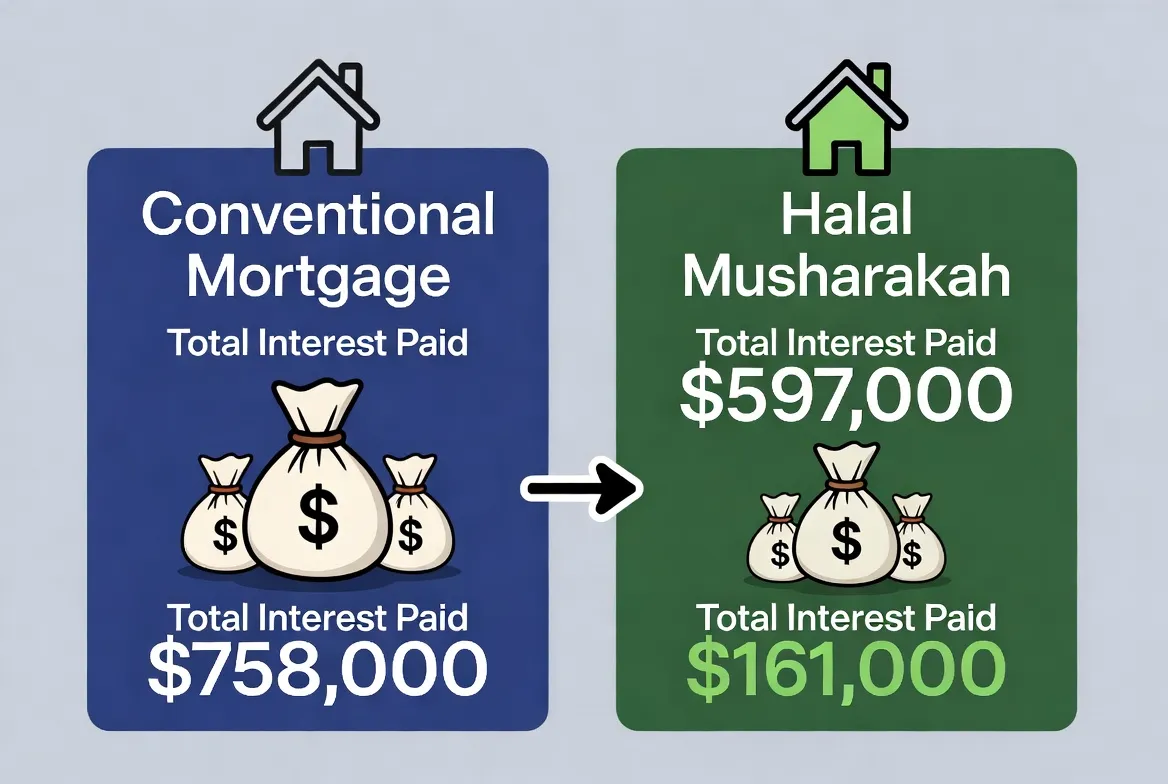

Halal Mortgage vs Conventional Mortgage: The Real Numbers

This is what most people actually want to know.

On a $400,000 home purchase with a 20% down payment:

Conventional Mortgage (6.9%) Total Cost: $758,660

Halal Musharakah (7.0% profit rate) Total Cost: $597,800

Estimated Savings: $160,860

The halal mortgage payment starts slightly higher but decreases over time as your ownership increases. A conventional mortgage payment remains essentially unchanged throughout the term.

Who Qualifies for a Halal Mortgage in the US?

The qualification criteria for a halal mortgage closely mirror conventional mortgage underwriting.

Credit Score

Minimum 620–640 for most programs. Scores above 720 typically qualify for the best rates.

Down Payment

Typically 20%, though some providers offer lower down payment options under specific conditions.

Debt-to-Income Ratio

Generally between 43% and 50%.

Employment and Income

Standard documentation is required, including tax returns, pay stubs, and employment verification.

Property Types

Single-family homes, condos, townhomes, and certain multi-unit properties may qualify.

Religion

No religious affiliation is required. Halal mortgage providers serve people of all faiths and backgrounds.

How to Apply for a Halal Mortgage in the US (2026)

Step 1 — Run Your Numbers

Use a halal mortgage calculator to compare costs and estimate monthly payments.

Step 2 — Find Providers in Your State

Compare available providers, rates, minimum down payments, and financing structures.

Step 3 — Get Pre-Qualified

Contact multiple providers for a free pre-qualification review and financing estimate.

Step 4 — Submit Your Full Application

Provide income documentation, employment verification, asset statements, and property details.

Step 5 — Sign the Partnership Agreement

Instead of a traditional loan agreement, you sign a co-ownership or Islamic financing agreement.

Expect the closing process to take approximately 45–60 days.

Frequently Asked Questions

Is a Halal Mortgage More Expensive Than a Conventional Mortgage?

The initial monthly payment may be slightly higher. However, the total cost over the life of the financing is often lower because no interest is charged.

Can Non-Muslims Get a Halal Mortgage?

Yes. Halal mortgages are available to all qualified buyers regardless of religion.

Is a Halal Mortgage Legal in the United States?

Yes. Islamic finance providers operate under US laws and regulations and offer legally recognized home financing products.

What Happens If I Miss a Payment?

The exact process depends on the provider and contract structure, but ownership-based arrangements are generally handled differently from conventional debt-based mortgages.

Which Halal Mortgage Lender Is Best?

The best lender depends on your state, credit profile, down payment amount, and financing needs. Comparing multiple providers is recommended.

The Bottom Line

A halal mortgage is not simply a religious alternative to a conventional mortgage. It is a different financial structure built around co-ownership, risk-sharing, and the elimination of interest.

For many buyers, it offers lower long-term costs, increasing ownership over time, and a financing model that aligns the interests of both parties.

It is available today in multiple US states and can be used by buyers of any faith.

Before applying, compare providers, review the financing structure carefully, and calculate the total long-term cost so you can make the best decision for your situation.