If you are comparing halal mortgage options right now, you need one thing before anything else: the actual current numbers. Here they are.

As of May 2026, halal mortgage profit rates range from 6.74% to 7.85% depending on your provider, credit score, and down payment. The 30-year conventional fixed-rate average is 6.87% (Freddie Mac, May 2026 Primary Mortgage Market Survey). At current rates, the best-qualified halal mortgage buyers are accessing financing that is priced within 0–0.5% of the conventional market — while eliminating compound interest entirely over 30 years.

May 2026 Halal Mortgage Rate Table — All Major Providers

Provider | Structure | Best Rate (720+ FICO) | Standard Rate (680 FICO) | States |

|---|---|---|---|---|

Guidance Residential | Musharakah | 6.74% | 7.12% | 27 + DC |

Lariba Finance | Ijara-based | 6.85% | 7.18% | Nationwide |

UIF Corporation | Musharakah | 6.89% | 7.24% | 30+ |

IjaraCDC | Ijara | 6.95% | 7.28% | 15+ |

Devon Bank | Murabaha / Ijara | 7.10% | 7.45% | Nationwide |

Manzil | Musharakah | 7.25% | 7.55% | 7 |

Conventional 30yr Fixed | Interest loan | 6.49% | 6.87% | All 50 states |

Profit rates as of May 2026. Rates update regularly and vary by loan amount, property type, down payment, and state. Contact providers directly for a personalized quote. Conventional rate: Freddie Mac Primary Mortgage Market Survey, May 2026.

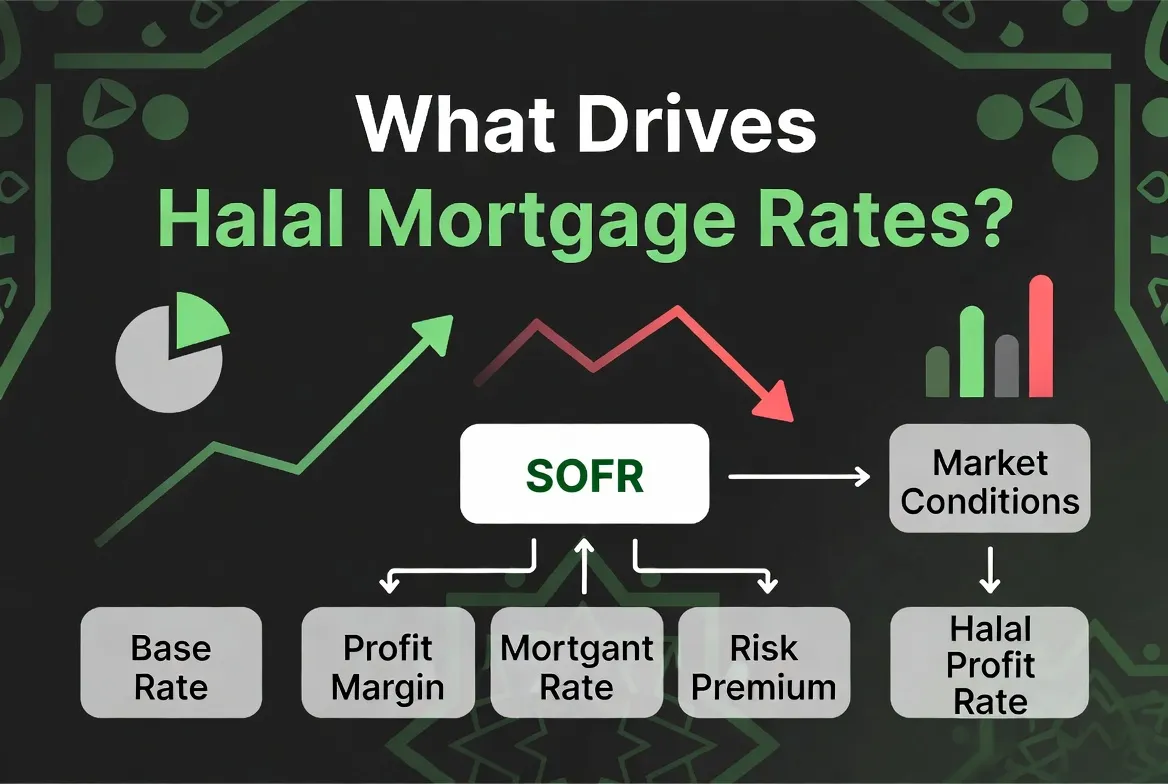

What Is Driving Halal Mortgage Rates Right Now

Most US halal mortgage profit rates are benchmarked to SOFR — the Secured Overnight Financing Rate, the Federal Reserve's replacement for LIBOR. SOFR sits at approximately 5.30% as of May 2026. Each lender adds a margin (typically 1.4–2.5%) to arrive at their published profit rate.

This matters for one practical reason: halal profit rates and conventional mortgage rates move in the same direction and at roughly the same time. When the Fed cuts rates, both fall. When the Fed raises rates, both rise. The difference is not in rate direction — it is in total cost structure. A halal profit rate of 7.0% costs dramatically less over 30 years than a conventional interest rate of 6.87%, because the halal structure eliminates compounding.

On a $400,000 home at current rates, the difference is approximately $159,000 in total payments over 30 years — despite the nominal profit rate being nearly identical to the conventional interest rate.

What Changed Since April 2026

Guidance Residential reduced its best-qualified profit rate by 0.12% in early May, following the Fed's decision to hold rates steady at its April meeting while signaling possible cuts in H2 2026. UIF Corporation held rates flat. Devon Bank slightly widened its spread on Murabaha products due to increased origination volume in Q1 2026.

The broader trend: halal mortgage profit rates have declined approximately 0.35% from their 2024 peak of around 7.4–7.8% for best-qualified borrowers. If the Fed delivers the two rate cuts it signaled at its May 2026 meeting, the best halal mortgage rates could reach the 6.25–6.50% range by Q4 2026.

Lock Now or Wait? The Honest Answer

This is the question every buyer asks, and it deserves an honest answer rather than a hedge.

Lock now if: You have found the right property, you qualify for a rate under 7.2%, and your financial situation is stable. The total cost advantage of Islamic financing exists at any rate level — the $159,000 savings versus conventional applies whether rates are 6.74% or 7.25%. Waiting for rates to fall while you hold off buying costs you in home price appreciation and continued rent payments that build zero equity.

Consider waiting if: You are still building your down payment, your credit score is below 680 (improving it by 40 points could save 0.25–0.50% on your rate), or you are genuinely uncertain about your employment stability. These are real financial reasons to pause — rate speculation is not.

The math on waiting: If rates fall 0.50% by Q4 2026 and you delay purchasing a $450,000 home by 6 months, you save approximately $14,000 in total interest over 30 years from the lower rate — but you also pay approximately $12,000–$18,000 in rent during those 6 months with zero equity return. The breakeven on waiting is much longer than most buyers realize.

How to Get the Best Halal Mortgage Rate Available to You

Four factors determine where in the rate range you land:

Credit score. The single biggest lever. A 720+ FICO score gets Guidance Residential's 6.74%. A 660 FICO score gets 7.20%+. If you are between 660 and 700, a 90-day credit improvement effort before applying is worth the time. Paying down revolving debt to under 30% utilization is the fastest improvement.

Down payment size. A 25–30% down payment versus the minimum 20% typically reduces your profit rate by 0.10–0.25%, depending on the provider.

Get quotes from at least 3 providers. Guidance Residential, UIF, and IjaraCDC are all competitive right now — and the spread between their best offers can be 0.20–0.40%. On a $400,000 financing, 0.20% is approximately $15,000 over 30 years. The 45 minutes it takes to get three pre-qualifications is the highest-ROI hour in your home purchase.

Rate lock timing. Once you have a property under contract, lock your rate immediately. Halal profit rates can move within a week of major Fed announcements. Most providers offer 30–60 day locks at no cost.

Frequently Asked Questions

Are halal mortgage rates higher than conventional rates right now?

At the best-qualified level (720+ FICO, 20% down), Guidance Residential's 6.74% profit rate is actually lower than the conventional average of 6.87% as of May 2026. At standard qualification levels (680 FICO), halal rates (7.12%–7.28%) are 0.25–0.40% above the conventional average. However, the nominal rate comparison is misleading — a halal profit rate of 7.0% costs significantly less over 30 years than a conventional interest rate of 6.87% because the halal structure eliminates compound interest. Always compare total 30-year cost, not just the headline rate.

How often do halal mortgage rates update?

Most providers update their published profit rates weekly, following movements in SOFR and the broader rate environment. Rates can change between when you receive a pre-qualification estimate and when you lock — always confirm the rate in writing and lock as soon as you are under contract on a property. This rate table is updated monthly.

Does my credit score affect my halal mortgage rate the same way as conventional?

Yes — the credit score impact on halal profit rates is nearly identical to conventional mortgage rate pricing. The difference between a 620 FICO score and a 720 FICO score is approximately 0.50–0.75% in profit rate, which translates to roughly $38,000–$57,000 in total cost on a $400,000 home over 30 years. If your score is below 700, spending 60–90 days improving it before applying is a high-value investment of time.

Use our free Halal Mortgage Calculator to compare your total 30-year cost at current rates — enter your home price, down payment, and state to see exactly what you save versus a conventional mortgage.

For the complete guide to halal mortgage structures, providers, and the full application process, read the Halal Mortgage USA 2026 Guide. To find every verified provider in your state with current rates, visit our State Finder.

This rate table will be updated in the first week of every month. Subscribe to Halal Market Watch to get the updated rate table delivered to your inbox every Friday — including rate change alerts when a major provider moves.