Most buyers researching halal mortgages quickly narrow down to two names: Guidance Residential and UIF Corporation. These are the two largest dedicated Islamic home financing providers in the United States. Both offer Musharakah co-ownership structures. Both are NMLS-licensed. Both have been operating for over 20 years.

The question is not whether they are legitimate — they both are. The question is which one is right for your specific situation. This comparison gives you the direct answer.

The Quick Verdict (Expand Below for Detail)

Choose Guidance Residential if...

You have W-2 employment income

Your credit score is 720 or above

You want the lowest possible profit rate

You live in CA, TX, VA, MD, NJ, NY, or DC area

You can only put 5%–10% down

You want the most established lender track record

Choose UIF Corporation if...

You are self-employed or have non-traditional income

Your credit score is in the 620–700 range

You need more flexible underwriting criteria

You live in MI, OH, IN, or other Midwest states

You have 20% down and want broader state access

You want an FDIC-insured bank parent institution

If neither column clearly matches your situation, read the full comparison below — it gets more specific.

Provider Profiles

Guidance Residential

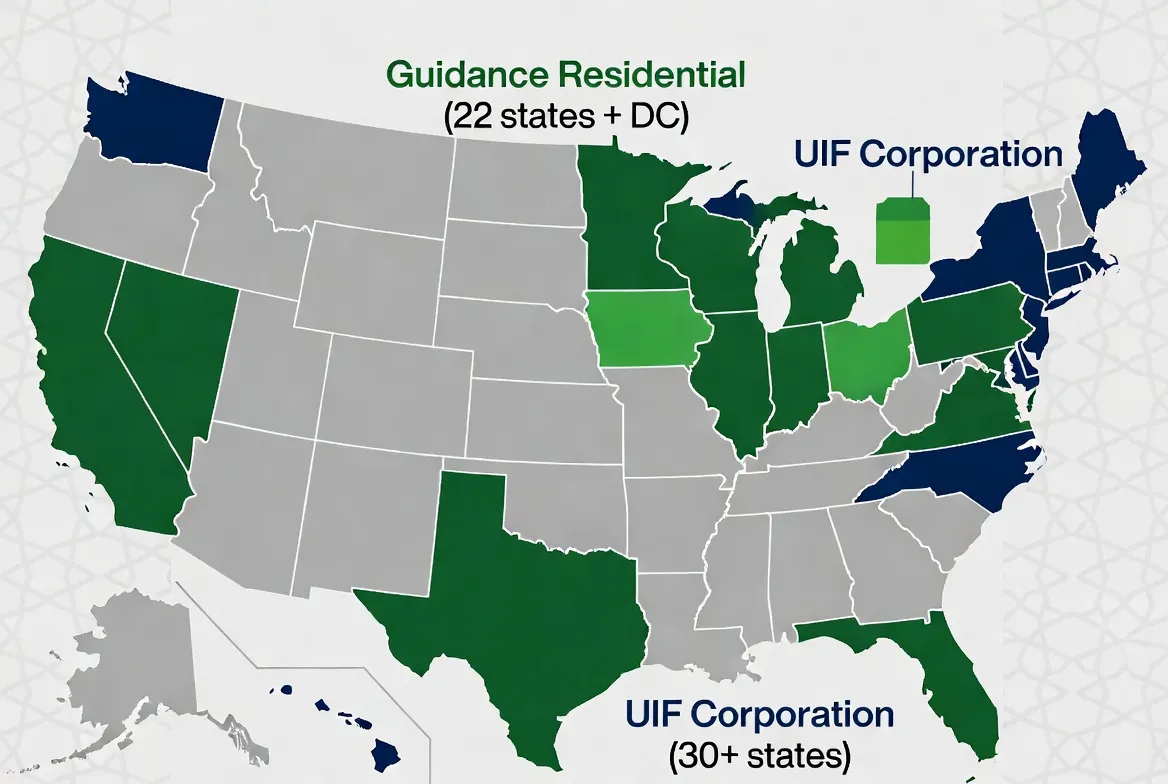

Founded in 1999 and headquartered in Reston, Virginia, Guidance Residential is the largest dedicated Islamic home financing company in the United States. They have completed over 50,000 home financings since inception — more than all other US Islamic mortgage providers combined. Their Sharia supervisory board includes Sheikh Yusuf Talal DeLorenzo, one of the most respected Islamic finance scholars in North America. They operate in 22 states plus DC.

Freddie Mac approved Guidance's Musharakah product structure in 2001 — a milestone that gave the product secondary market access and legitimacy that no other Islamic lender had at the time. Fannie Mae has also accepted their structure. This secondary market access is part of why Guidance can offer the most competitive rates among US Islamic lenders.

UIF Corporation (University Islamic Financial)

Founded in 2003 and headquartered in Ann Arbor, Michigan, UIF Corporation is a subsidiary of University Bank — an FDIC-insured community bank. This parent bank structure means UIF customer deposits are federally insured, and the company operates under full bank holding company oversight in addition to NMLS licensing. UIF serves 30+ states — a broader geographic footprint than Guidance — and is particularly dominant in Michigan, Ohio, Indiana, and the wider Midwest.

UIF has built a strong reputation specifically for working with self-employed Muslim professionals and business owners whose income documentation does not fit the standard W-2 template that conventional underwriters (and, to a degree, Guidance) prefer.

Head-to-Head: Every Dimension That Matters

Dimension | Guidance Residential | UIF Corporation |

|---|---|---|

Founded | 1999 | 2003 |

Headquarters | Reston, Virginia | Ann Arbor, Michigan |

Parent institution | Guidance Financial Group | University Bank (FDIC-insured) |

Total financings completed | 50,000+ | ~15,000+ |

States served | 22 states + DC | 30+ states |

Structure offered | Diminishing Musharakah | Diminishing Musharakah |

Best rate (720+ FICO, May 2026) | 6.74% | 6.89% |

Standard rate (680 FICO) | 7.12% | 7.24% |

Minimum credit score | 620 | 620 |

Minimum down payment | 5% (qualifying borrowers) | 20% |

Self-employed income | Accepted; stricter documentation | Accepted; more flexible |

Investment properties | Yes (25% down typical) | Yes (25% down typical) |

Commercial real estate | Yes | Yes |

Closing timeline | 45–55 days | 45–60 days |

Fannie / Freddie approved | Yes — both | Yes — both |

Sharia board | Sheikh Yusuf Talal DeLorenzo + board | Independent Sharia committee |

The Rate Difference — What It Actually Costs You

Guidance's best rate is 6.74% vs UIF's 6.89% — a 0.15 percentage point difference. On a $320,000 finance amount over 30 years, this difference costs approximately:

Month 1 payment difference: ~$40/month (Guidance lower)

Total 30-year cost difference: ~$8,200 (Guidance lower)

$8,200 is real money — but it matters less than finding the lender who can actually approve your application. A 0.15% rate advantage means nothing if the lender rejects you due to income documentation requirements. For self-employed buyers, UIF's flexibility often outweighs Guidance's rate edge.

The Self-Employed Question

This is where the two lenders diverge most meaningfully. A significant proportion of American Muslim homebuyers are business owners, doctors with their own practices, engineers on contract, or other self-employed professionals. Their income is real — often higher than equivalent W-2 employees — but their tax returns show different figures than their actual cash flow, because business deductions reduce taxable income.

Guidance Residential uses standard mortgage underwriting that relies heavily on two years of tax returns. For self-employed buyers who aggressively deduct business expenses, this can result in the lender seeing income that is 30–50% lower than the buyer's actual cash position. Guidance has been improving its self-employed documentation process, but it remains more rigid than UIF.

UIF Corporation has invested specifically in underwriting self-employed and non-traditional income applicants. They accept bank statement loans (12–24 months of business bank statements showing actual deposits), 1099 income, and some alternative income documentation forms. For a Muslim business owner whose tax return shows $95,000 but whose bank statements show $280,000 in annual deposits, UIF's program may produce approval where Guidance cannot.

Geographic Coverage: Where Each Lender Operates

This is the most practical deciding factor for many buyers. If only one of these lenders serves your state, the comparison ends here.

State | Guidance Residential | UIF Corporation |

|---|---|---|

California | ✅ Yes | ✅ Yes |

Texas | ✅ Yes | ✅ Yes |

Michigan | ✅ Yes | ✅ Yes (strongest market) |

Virginia / DC Metro | ✅ Yes (HQ state) | ✅ Yes |

New York / New Jersey | ✅ Yes | ✅ Yes |

Maryland | ✅ Yes | ✅ Yes |

Illinois | ✅ Yes | ✅ Yes |

Ohio | ✅ Yes | ✅ Yes (strong presence) |

Indiana | ❌ Not currently | ✅ Yes |

Wisconsin | ✅ Yes | ✅ Yes |

Tennessee | ❌ Not currently | ✅ Yes |

Connecticut | ❌ Not currently | ✅ Yes |

Missouri | ❌ Not currently | ✅ Yes |

If you live in Indiana, Tennessee, Connecticut, Missouri, or several other states, UIF serves you and Guidance does not. The decision is made for you.

The Down Payment Difference

Guidance Residential offers financing programs starting at 5% down for qualifying borrowers. This is a significant advantage for first-time buyers who have not yet accumulated 20%. On a $400,000 home, 5% down is $20,000 vs 20% down at $80,000 — a $60,000 difference in cash required at closing.

UIF Corporation requires a minimum 20% down payment on all programs. If you have less than 20% saved and Guidance serves your state, Guidance is your only Islamic mortgage option among these two providers.

What Buyers Say: Application Experience

Based on buyer feedback across Islamic finance communities:

Guidance Residential has a polished, well-resourced application process — dedicated loan officers in most major markets, strong digital tools, and a team experienced in explaining the co-ownership structure to real estate agents and title companies.

UIF Corporation has a more relationship-driven process — particularly in Michigan, where they have deep community ties. Their loan officers are consistently cited for flexibility and willingness to problem-solve non-standard situations.

The Honest Limitations of Each

Guidance's limitation: The 22-state coverage is the primary constraint. Their stricter self-employed documentation also eliminates some applicants who UIF would approve.

UIF's limitation: The 20% minimum down payment requirement excludes first-time buyers who have not yet saved a full 20%. Their profit rates are also slightly higher than Guidance.

Our Recommendation by Buyer Profile

Your Situation | Recommended Lender | Why |

|---|---|---|

First-time buyer, less than 20% down, 720+ credit, W-2 income | Guidance Residential | Only option with sub-20% down; best rates for strong credit |

Self-employed buyer, 20%+ down, complex income docs | UIF Corporation | More flexible underwriting; bank statement programs |

Michigan, Ohio, Indiana buyer with 20% down | UIF Corporation | Dominant Midwest presence; community relationships |

California, Texas, Virginia, DC Metro buyer, W-2 income | Guidance Residential | Strongest presence; most competitive rates |

720+ credit, 20%+ down, W-2 income, served by both | Get quotes from both | Rate difference is the deciding factor |

State served only by UIF | UIF Corporation | Only option — contact immediately |

The Bottom Line

Guidance Residential is the right choice for most buyers in the major metro markets it serves — its rate advantage, 5% down option, and 25-year track record make it the strongest all-around option when it is available to you.

UIF Corporation is the right choice when Guidance does not serve your state, when your income is self-employed or non-traditional, or when you are buying in the Midwest where UIF's community presence and local expertise runs deep.

For most buyers in states where both operate: get pre-qualification quotes from both. It is free, takes 15 minutes each, and the actual rate offer they give you is what you should compare.

Frequently Asked Questions

Is Guidance Residential or UIF Corporation better?

Neither is universally better — the right choice depends on your state, income type, and down payment. Get quotes from both if they both serve your state.

Does Guidance Residential require 20% down?

No — Guidance Residential offers programs starting at 5% down for qualifying borrowers. UIF Corporation requires a minimum 20% down payment.

Are both Guidance Residential and UIF Corporation Sharia-compliant?

Yes — both use diminishing Musharakah structures reviewed and certified by independent Sharia supervisory boards. Both are Fannie Mae and Freddie Mac approved.

Can I apply to both Guidance and UIF at the same time?

Yes — and for buyers served by both, this is the recommended approach. Pre-qualifications involve only a soft credit pull.

Use our free Halal Mortgage Calculator to model what your monthly payment looks like at Guidance's 6.74% vs UIF's 6.89% on your specific home price and down payment.

To see which providers operate in your specific state — including Guidance, UIF, Devon Bank, IjaraCDC, and Lariba — visit our State Finder. For the complete guide to halal mortgage structures, rates, and the application process, read the Halal Mortgage USA 2026 Guide.