Calculating zakat should not require a degree in Islamic jurisprudence. It requires four things: knowing the current nisab threshold, knowing what counts as zakatable, knowing what to deduct, and multiplying the result by 2.5%. This guide gives you all four — including a complete line-by-line worked example for a typical American Muslim household.

If you want to skip the explanation and go straight to the calculation, use our Zakat Calculator — it handles every asset type below automatically with current 2026 nisab values built in.

Before You Start: Two Things You Need to Know

1. Your Zakat Anniversary Date (Hawl)

Zakat is due once per lunar year after your wealth has continuously exceeded the nisab for a full 354-day lunar year. Your "hawl" is the anniversary date — it is personal to you, not a universal date.

Many American Muslims calculate zakat during Ramadan because the spiritual reward is multiplied in that month. This is valid and recommended. If your hawl date is actually in Sha'ban (the month before Ramadan), paying during Ramadan means you are paying approximately 30 days early — which is permissible (it is charity given ahead of its due date, which scholars allow).

If you have never calculated zakat before and are starting this year, your hawl begins the first day your wealth exceeds the nisab threshold. Your first zakat payment is due one lunar year from that date.

2. The 2026 Nisab Threshold

The nisab is the minimum wealth level at which zakat becomes obligatory. It is defined in weight of gold or silver — not in dollars — so it changes as metal prices change.

Nisab Standard | Weight | Metal Price (May 2026) | 2026 USD Value |

|---|---|---|---|

Gold Nisab (most used in North America) | 87.48 grams (7.5 tola) | ~$3,200/troy oz | ~$9,020 |

Silver Nisab | 612.36 grams (52.5 tola) | ~$32/troy oz | ~$634 |

Verify current gold/silver prices at goldprice.org before calculating. The nisab is fixed in weight — not dollars. At $3,200/oz gold, the gold nisab is approximately $9,020. This changes monthly with gold prices.

Which nisab should you use?

Most North American scholars and Islamic finance organizations — including ISNA, National Zakat Foundation USA, and Zakat Foundation of America — recommend the gold nisab for modern financial assets. The silver nisab at $634 would make zakat obligatory on almost any adult with a savings account, which was not the classical intent for who qualifies as a zakat payer.

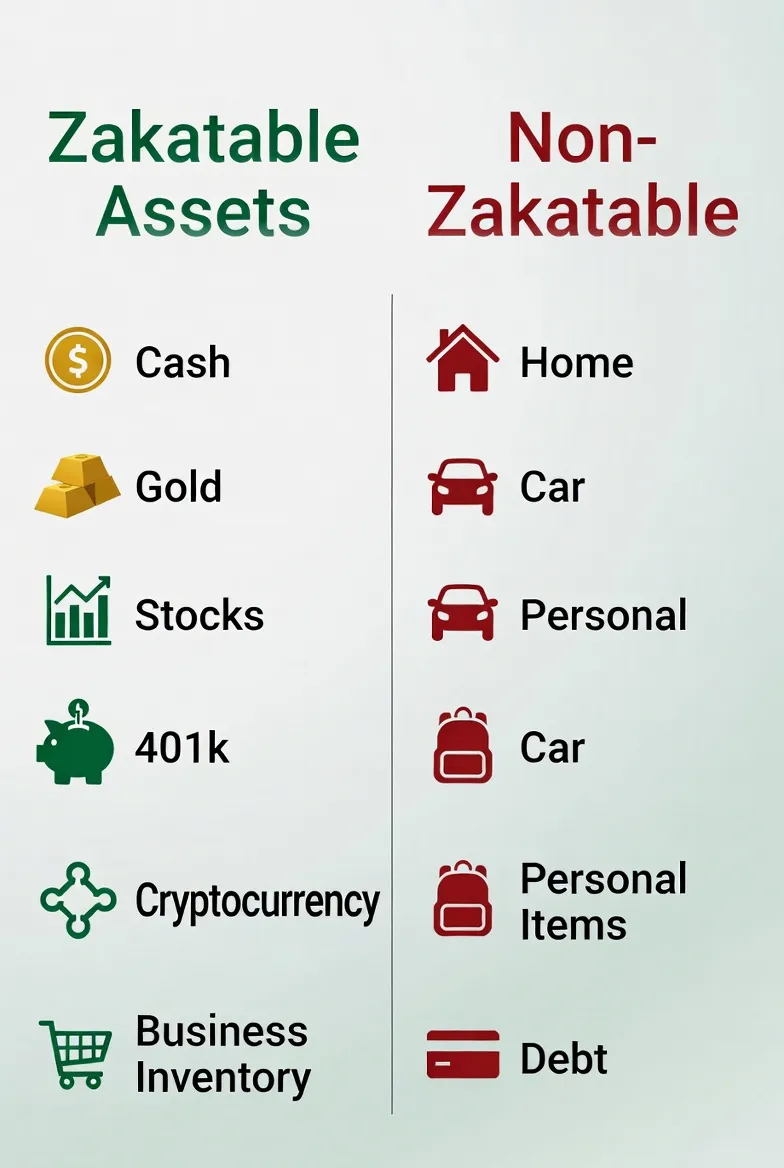

What Counts as Zakatable — Complete Asset List

Asset Type | Zakatable? | At What Value | Notes |

|---|---|---|---|

Cash (checking, savings, money market) | ✅ Yes | Full balance | Every dollar in every account |

Physical gold | ✅ Yes | Current market value | Coins, bars, any stored gold |

Gold jewelry (Hanafi school) | ✅ Yes — all of it | Current market value | Even if worn daily |

Gold jewelry (Maliki/Shafi'i/Hanbali) | ✅ Excess only | Current market value | Daily-wear personal jewelry exempt; stored/excess zakatable |

Physical silver | ✅ Yes | Current market value | Coins, bars, stored silver |

Stocks and ETFs (trading intent) | ✅ Yes | Full market value on zakat date | If held primarily to trade for profit |

Stocks and ETFs (long-term investment) | ✅ Yes — look-through basis | Zakatable assets per share × shares held | Zoya/Musaffa calculate this automatically; reduces liability |

Roth IRA balance | ✅ Yes (majority view) | Full balance | Accessible after 59½ without penalty; fully zakatable |

401k / Traditional IRA | ✅ Yes — net of penalty | Balance × 70% (est. after 10% penalty + tax) | Most contemporary scholars: deduct estimated withdrawal costs |

Business cash and inventory | ✅ Yes | Cash + inventory market value + receivables | Only liquid/near-liquid assets; equipment excluded |

Money owed to you (receivables) | ✅ Yes — if likely to collect | Full amount | Exclude if very unlikely to collect |

Primary home you live in | ❌ No | — | Real estate for personal use is exempt |

Rental property | ❌ No (property itself) | — | The property is not zakatable; rental income received IS |

Car, personal belongings | ❌ No | — | Personal use items exempt |

Business equipment, buildings | ❌ No | — | Fixed assets not zakatable; only liquid business assets |

What to Deduct — Your Immediate Liabilities

Subtract debts that are currently due — not long-term outstanding balances:

✅ Deduct: Credit card balance due this billing cycle

✅ Deduct: Bills, rent, or utilities due within the month

✅ Deduct: One year of mortgage installments (not the full outstanding balance)

✅ Deduct: Any other debt payments coming due immediately

❌ Do NOT deduct: The full remaining balance of your 30-year mortgage

❌ Do NOT deduct: Future car loan payments not yet due

❌ Do NOT deduct: Student loans not currently in repayment

The most common mistake: deducting the entire remaining mortgage balance ($280,000) from zakatable wealth, leaving zero zakat liability. Most contemporary scholars do not permit this. You may deduct the mortgage payments due within the current year — not the full outstanding long-term balance.

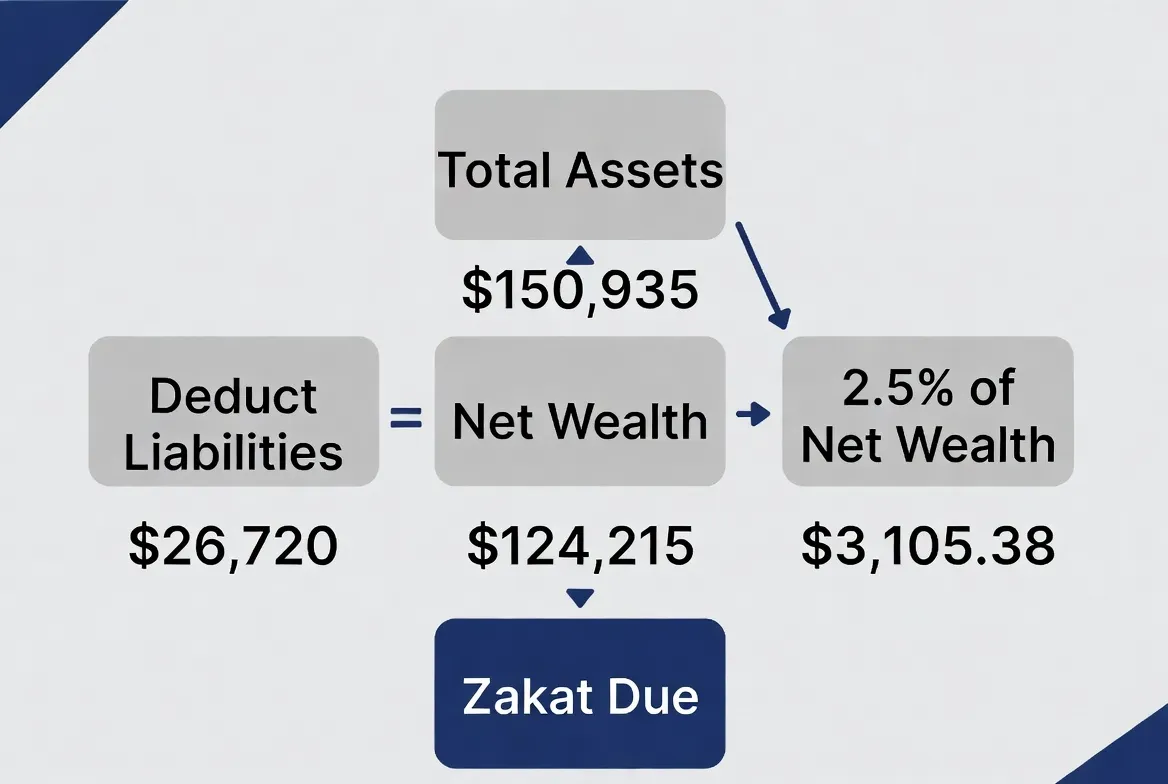

The Zakat Calculation Formula

Zakat = (Total Zakatable Assets − Immediate Liabilities) × 2.5%

This only applies if the net result exceeds the nisab (~$9,020 using gold standard, May 2026).

Complete Worked Example — Step by Step

Here is a complete calculation for a real scenario: a Muslim American professional, age 38, married, employed as an engineer with a 401k, some savings, an ETF investment account, and gold jewelry. Follow along with your own numbers.

Step 1 — List Every Zakatable Asset

Asset | Balance / Value | Zakatable Amount | Notes |

|---|---|---|---|

Checking account (Chase) | $6,200 | $6,200 | Full balance on zakat date |

Savings account (Marcus) | $28,500 | $28,500 | Full balance |

Emergency fund (HYSA) | $15,000 | $15,000 | Full balance — it is cash regardless of its purpose |

SPUS ETF in Roth IRA (300 shares × $58) | $17,400 | $17,400 | Full market value (long-term hold; could also use look-through) |

401k balance (Fidelity) | $112,000 | $78,400 | $112,000 × 70% = $78,400 (net of est. 10% penalty + ~20% tax) |

Gold jewelry (Hanafi, 45 grams) | 45g × $103/g = $4,635 | $4,635 | All gold jewelry zakatable under Hanafi; skip if Maliki/Shafi'i daily-wear |

Money owed by friend (likely to repay) | $800 | $800 | Include expected receivables |

Primary home | $480,000 | $0 | Personal residence — exempt |

Car | $32,000 | $0 | Personal use — exempt |

TOTAL ZAKATABLE ASSETS | $150,935 |

Step 2 — Subtract Immediate Liabilities

Liability | Amount to Deduct | Notes |

|---|---|---|

Credit card balance due this month | $2,340 | Full balance — due now |

Utility bills due this week | $380 | Immediate liability |

One year of mortgage installments | $24,000 | $2,000/mo × 12 — one year only, not full balance |

Remaining mortgage balance ($265,000) | $0 | Long-term — do NOT deduct the full balance |

TOTAL DEDUCTIONS | $26,720 |

Step 3 — Calculate Net Zakatable Wealth

$150,935 − $26,720 = $124,215

This exceeds the gold nisab of approximately $9,020. Zakat is obligatory.

Step 4 — Calculate Zakat Due

$124,215 × 2.5% = $3,105.38

This household owes approximately $3,105 in zakat for 2026.

Step 5 — Pay Before the Hawl Deadline

Zakat can be paid in a lump sum or in installments throughout the year before the next hawl. Many families set up a monthly transfer of $258.78/month ($3,105 ÷ 12) to a zakat-eligible charity so the obligation is met continuously without a large annual payment.

The Three Tricky Assets — Detailed Guidance

Stocks and ETFs: Full Value vs Look-Through

You have two valid approaches for ETFs like SPUS or HLAL:

Full market value (simpler): Pay 2.5% of your total portfolio value on your zakat date. This is more conservative but simpler. Most practical for investors with under $50,000 in ETFs.

Look-through method (more precise): Pay 2.5% of only the zakatable assets underlying each stock or ETF — the cash, receivables, and inventory the company holds, proportional to your ownership. This typically reduces your zakat liability by 40–70% compared to paying on full market value. Zoya calculates this automatically for individual stocks. SP Funds publishes a zakatable amount per share for SPUS annually.

Both positions have valid scholarly basis. For ETF investors who want to use the look-through method, check the fund's annual Sharia report for the published zakatable amount per share. If not published, use full market value.

401k: The Three Scholarly Positions

There is genuine scholarly disagreement on 401k zakat. Three positions exist:

Position 1 — Full balance (most conservative): Pay 2.5% on the full 401k balance. The money is yours even if temporarily restricted.

Position 2 — Net of penalty (most common in North America): Pay 2.5% on the balance minus the estimated 10% early withdrawal penalty and estimated income tax. For most people, this means multiplying the balance by 70% (100% − 10% penalty − 20% estimated tax = 70%). This is the position recommended by most North American zakat organizations.

Position 3 — Upon receipt (most lenient): Pay no zakat on 401k funds until you actually receive distributions. The restriction on access means the wealth is not truly in your possession.

Our Zakat Calculator allows you to select which position to apply and calculates accordingly.

Gold Jewelry: The School Difference

Hanafi school (dominant in South Asia, Turkey, Central Asia): All gold jewelry is zakatable — even pieces worn daily. Calculate at current market value of the gold content (not the retail or resale price of the piece).

Maliki, Shafi'i, Hanbali schools: Gold jewelry worn regularly for personal use is exempt. Only stored, excess, or investment jewelry is zakatable.

Follow your madhab. If unsure, the Hanafi position (pay on all gold jewelry) is the more cautious approach.

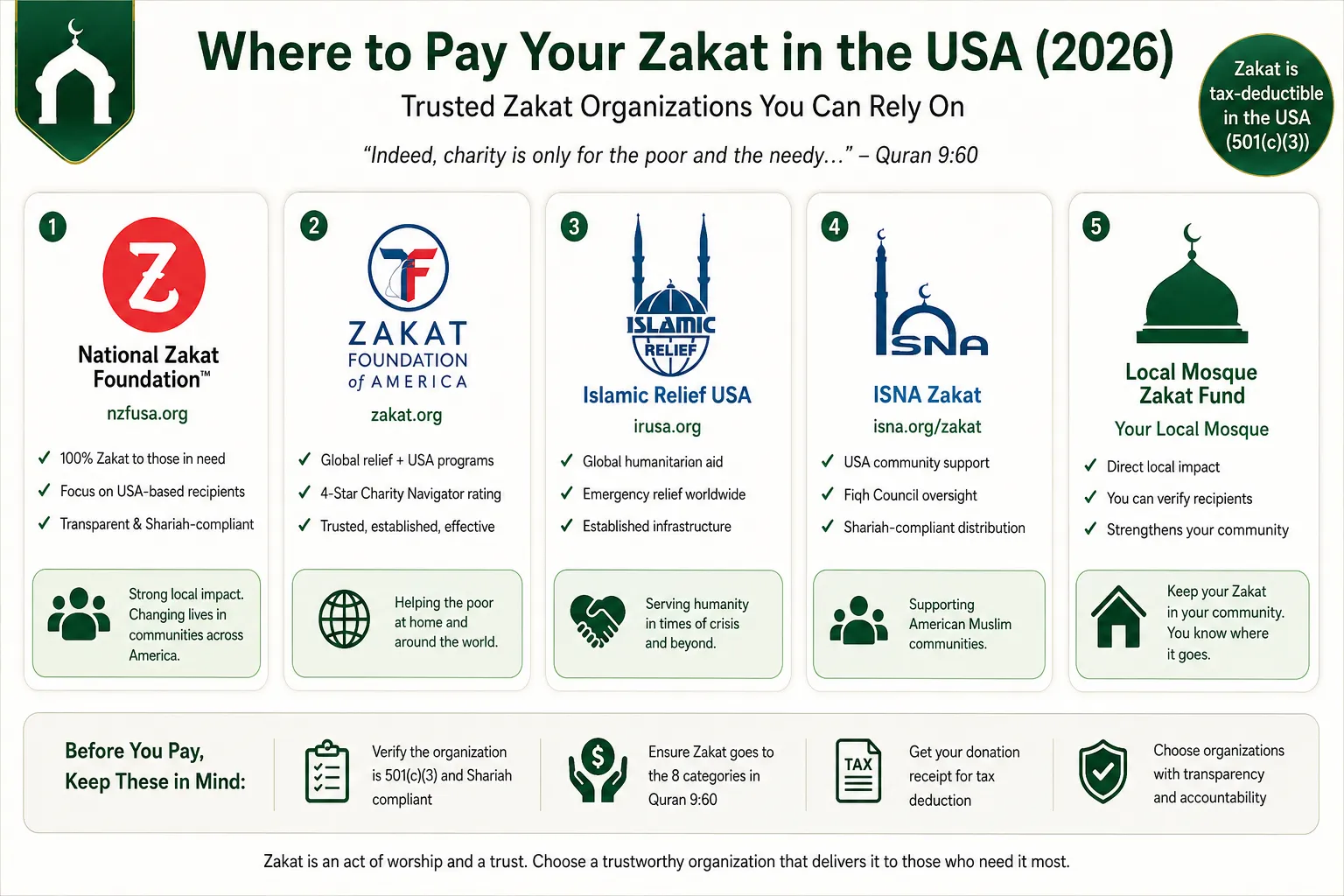

Where to Pay Your Zakat

Zakat must go to one of the eight categories defined in Quran 9:60 — the poor, the needy, zakat administrators, debtors, travelers in hardship, and others. Verified US zakat organizations:

National Zakat Foundation USA (nzfusa.org) — focuses on US-based recipients only; strong local impact

Zakat Foundation of America (zakat.org) — global relief + US domestic; 4-star Charity Navigator rating

Islamic Relief USA (irusa.org) — global humanitarian; established infrastructure

ISNA Zakat — US community support; Fiqh Council oversight

Local mosque zakat fund — direct local impact; you can verify recipient eligibility personally

Zakat paid to 501(c)(3) organizations is tax-deductible on your federal return. Zakat paid directly to individuals (even if they qualify) is not tax-deductible.

Common Mistakes That Change Your Calculation

Mistake | The Correct Approach |

|---|---|

Deducting the full remaining mortgage balance | Deduct one year of mortgage payments only (monthly × 12) |

Forgetting the 401k entirely | 401k is zakatable — at minimum pay on 70% of the balance |

Calculating on income instead of wealth | Zakat is on total accumulated wealth — not your annual salary |

Using a calendar year instead of lunar year | The hawl is 354 days — 11 days shorter than a solar year |

Forgetting money others owe you | Receivables you expect to collect are zakatable assets |

Not including the emergency fund | The emergency fund is cash — it is fully zakatable regardless of its purpose |

Calculating on stock purchase price, not current value | Zakat is on current market value on the zakat date — not what you paid |

Frequently Asked Questions

What is the zakat percentage in 2026?

Zakat is exactly 2.5% of your net zakatable wealth — unchanged from any other year. The rate has been fixed at 2.5% (1/40th) since the time of the Prophet Muhammad (peace be upon him) and applies to all categories of financial assets: cash, gold, silver, stocks, business inventory, and receivables. What changes annually is the nisab threshold in USD, because it is pegged to the price of gold and silver.

What is the nisab for zakat in 2026?

Using the gold standard (recommended by most North American scholars), the nisab in May 2026 is approximately $9,020 — calculated as 87.48 grams of gold at approximately $103/gram ($3,200/troy oz). Using the silver standard, the nisab is approximately $634. If your total net zakatable wealth exceeds the nisab you use, zakat is obligatory at 2.5%.

Do I pay zakat on money I owe in debt?

Debt reduces your zakatable wealth — but only the portion currently due, not your entire outstanding balance. If you have a $3,000 credit card balance due this month, deduct $3,000 from your zakatable assets. If you have $240,000 remaining on a 30-year mortgage, most scholars permit deducting only your current-year mortgage payments (e.g., $24,000 for a $2,000/month payment) — not the full $240,000 outstanding balance.

Is zakat on my salary or my savings?

Zakat is on your accumulated wealth — not your salary or annual income. Your salary becomes part of your zakatable wealth once you receive it and it sits in your accounts. If you earn $10,000 and spend $10,000 every month, you may have zero zakatable wealth even on a strong income. If you earn $80,000 and save $40,000 over the year, your zakat is calculated on your total accumulated savings and investments on your zakat anniversary date — not on the $80,000 you earned.

What if I missed paying zakat in previous years?

You are obligated to estimate and pay the missed zakat for every year you met the qualifying conditions. Calculate your approximate zakatable wealth for each missed year at 2.5% and pay what you owe. This is treated as a debt that must be discharged — it does not disappear with time. If paying everything at once is financially impossible, pay what you can now and make a committed plan to clear the remainder. Many scholars recommend making this a priority before voluntary charity.

The calculation above covers the most common American Muslim asset situation — savings, ETFs, 401k, and gold jewelry. If your situation includes business assets, rental income, agricultural income, or significant cryptocurrency holdings, additional rules apply.

Use our free Zakat Calculator to calculate your exact 2026 zakat obligation — it handles every asset type above, applies the current nisab threshold automatically, and lets you choose your scholarly position on 401k calculation. Takes under 5 minutes.

For the complete scholarly framework — all eight recipient categories, the three scholarly positions on retirement accounts, and how to calculate purification alongside zakat — read our full Zakat Guide.