You have decided you want a halal ETF. You have narrowed it down to SPUS or HLAL. You want to know which one to buy and why — not a list of factors to consider, but an actual answer.

Here it is upfront: Buy SPUS as your core halal ETF. Buy HLAL as a secondary holding if you want methodology diversification and broader mid-cap exposure.

The rest of this post explains exactly why — including the one technical difference between them that no other comparison article explains, and the specific situations where HLAL is actually the better choice.

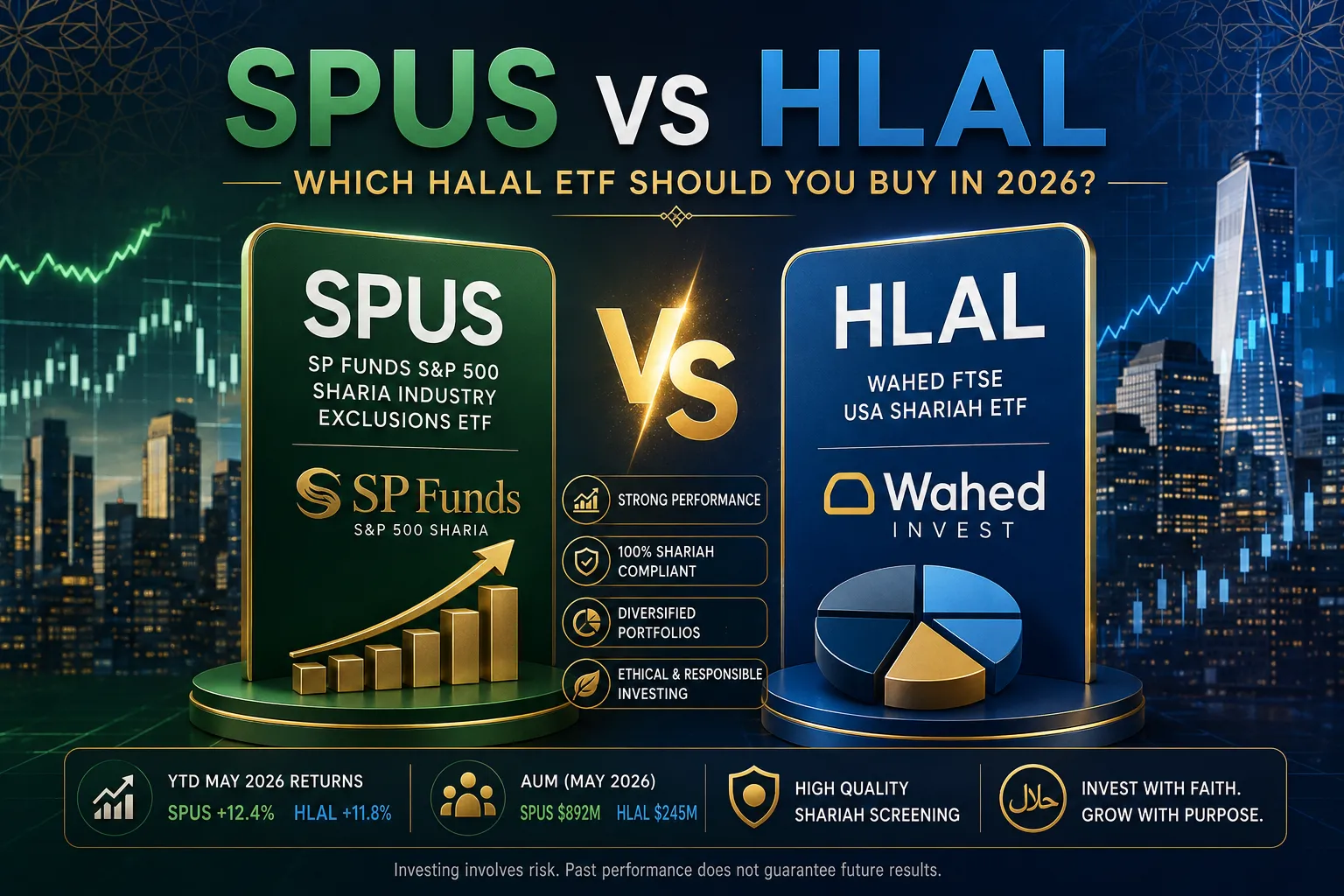

The Quick Numbers (May 2026)

Metric | SPUS | HLAL |

|---|---|---|

Full Name | SP Funds S&P 500 Sharia Industry Exclusions ETF | Wahed FTSE USA Shariah ETF |

Issuer | SP Funds (Saturna Capital affiliate) | Wahed Invest |

AUM (May 2026) | $892 million | $245 million |

Expense Ratio | 0.49% | 0.50% |

Underlying Index | S&P 500 Sharia Exclusions Index | FTSE USA Shariah Index |

Sharia Board | Ratings Intelligence Partners | Amanie Advisors |

Holdings Count | ~290 | ~320 |

Holdings Overlap | ~85% of holdings shared | |

Q1 2026 Return | +8.2% | +7.8% |

YTD May 2026 | +12.4% | +11.8% |

S&P 500 (SPY) YTD | +10.9% — both halal ETFs beat it | |

Inception Date | December 2019 | July 2019 |

Exchange | NYSE Arca | NYSE Arca |

Purification (2025, per share) | $0.18 | $0.14 |

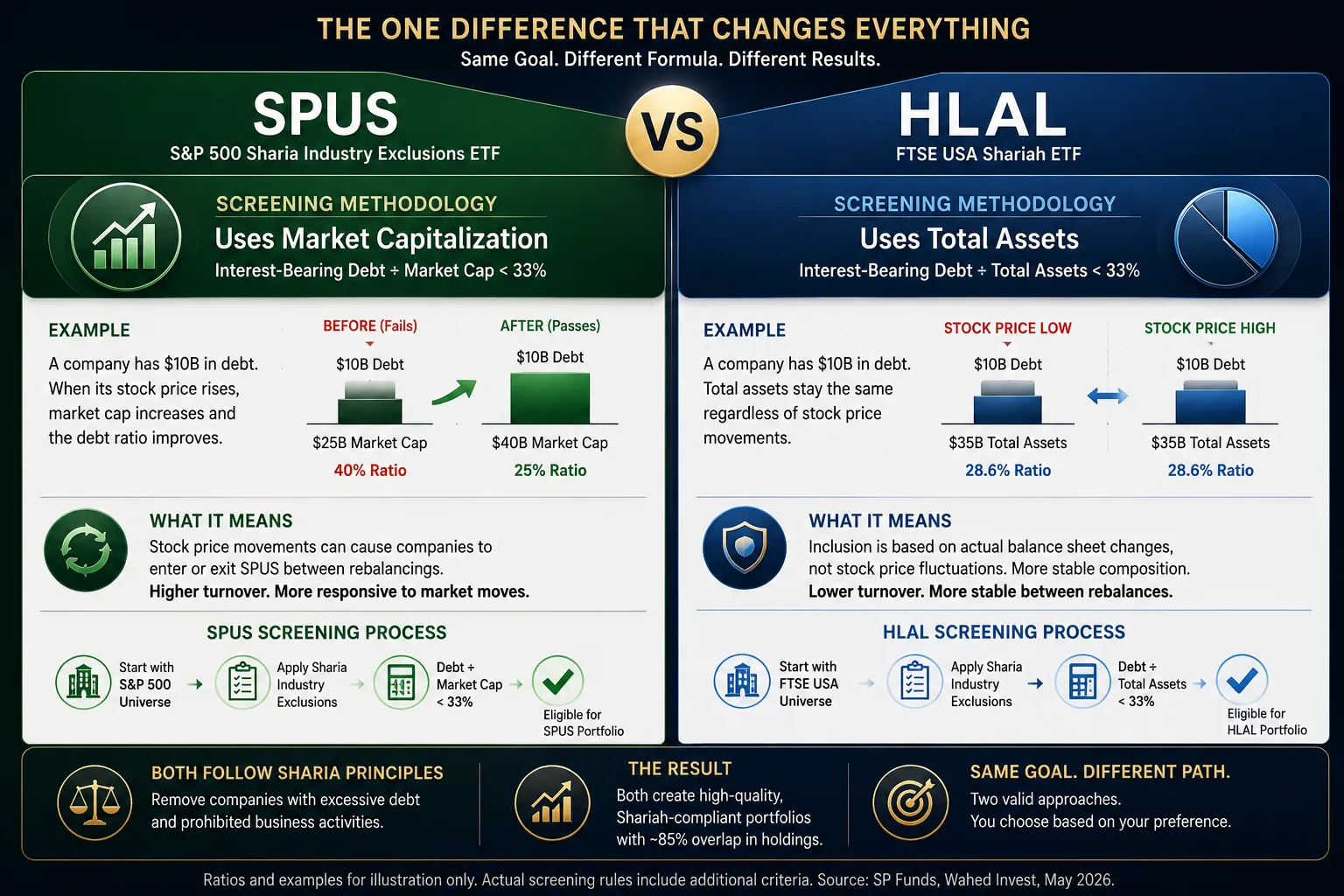

The One Difference No One Explains

Every comparison article covers AUM and expense ratio. None of them explain the actual structural difference between SPUS and HLAL — the one that determines which stocks are in each fund.

Both funds apply a financial ratio screen to eliminate companies with excessive interest-bearing debt. The key test: a company's interest-bearing debt must be under 33% of a specified denominator.

SPUS uses market capitalization as the denominator.

HLAL uses total assets as the denominator.

This sounds minor. It is not. Here is what it means in practice:

The Market Cap Problem (SPUS)

When a company's stock price rises, its market cap increases. If the company has $10 billion in debt and its market cap goes from $25 billion to $40 billion, its debt/market cap ratio falls from 40% (fails) to 25% (passes). The company now enters SPUS — even though its actual debt hasn't changed.

When that same company's stock price falls in a market downturn, its market cap drops from $40 billion back to $25 billion. Its debt/market cap ratio rises back to 40%. It gets removed from SPUS at the next rebalancing.

Result: SPUS's composition can shift meaningfully between quarterly rebalancings based on stock price movements — not just actual changes in company fundamentals.

Why HLAL's Method Is More Stable (But Has Its Own Trade-off)

Total assets don't change with daily stock prices. A company with $10 billion in debt and $35 billion in total assets has a 28.6% ratio — and that ratio stays the same whether the stock trades at $50 or $500. Inclusion/exclusion is driven by actual balance sheet changes, not market sentiment.

The trade-off: total assets can be inflated by goodwill, intangibles, and accounting items that don't reflect real economic value as clearly as market cap does. A company that made a large acquisition might have bloated total assets — making its debt ratio look lower than it economically is.

What This Means for You as an Investor

SPUS will have slightly higher turnover at quarterly rebalancings — more stocks entering and exiting based on price movements. This creates marginally higher transaction costs within the fund but also means SPUS quickly captures quality companies when they appreciate.

HLAL has more stable composition between rebalancings — the same companies tend to stay in until their actual financials change. This means fewer surprises but also potentially slower response to quality improvements in companies.

For a long-term buy-and-hold investor, this distinction is real but not decisive. Both methods produce high-quality Sharia-compliant portfolios. The 85% holdings overlap means you own essentially the same companies either way.

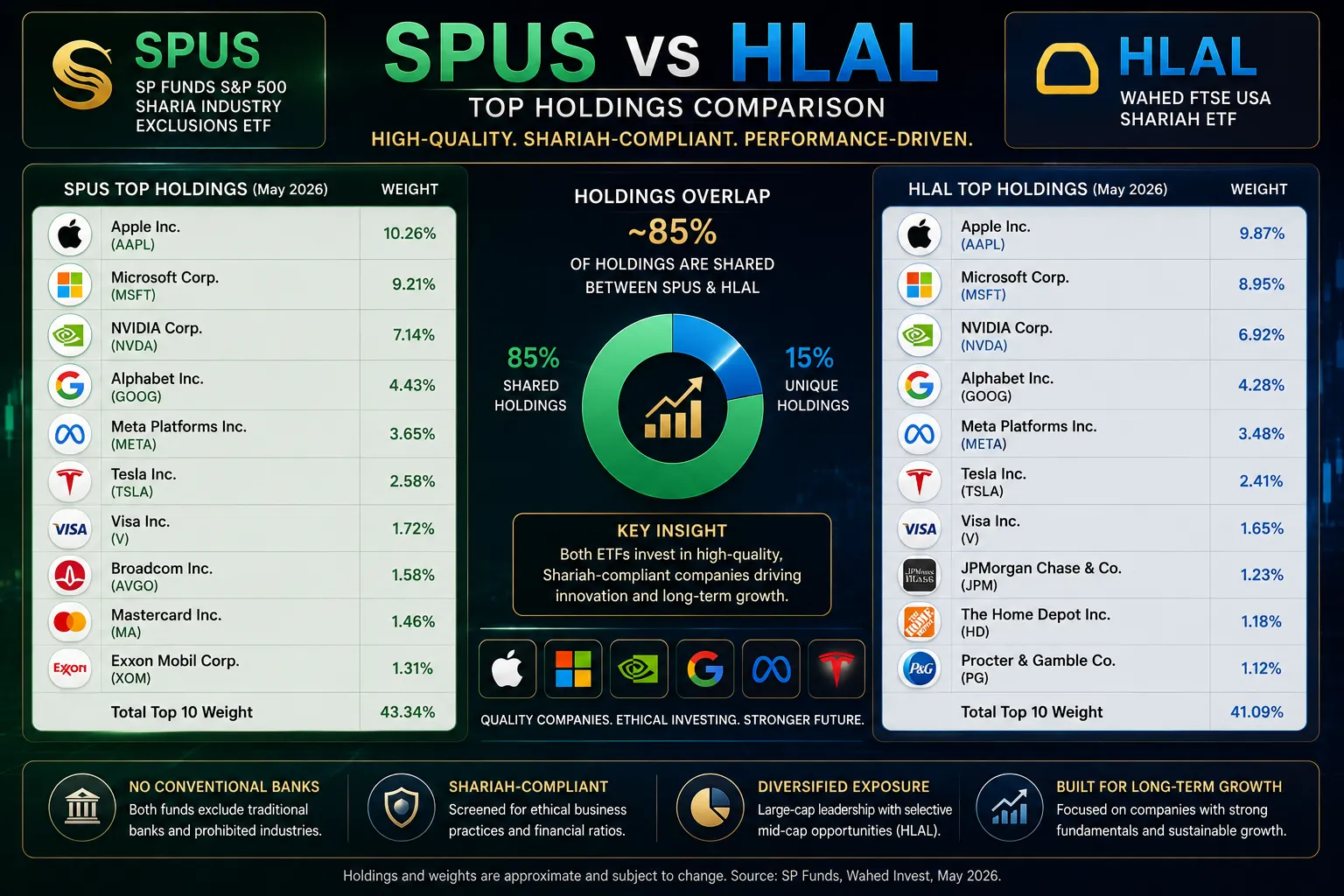

Holdings Comparison: What Each Fund Actually Owns

Company | In SPUS? | In HLAL? | Approx. Weight |

|---|---|---|---|

Apple (AAPL) | ✅ Yes | ✅ Yes | ~9–11% (largest holding both) |

Microsoft (MSFT) | ✅ Yes | ✅ Yes | ~8–10% |

Nvidia (NVDA) | ✅ Yes | ✅ Yes | ~6–8% |

Alphabet / Google (GOOG) | ✅ Yes | ✅ Yes | ~4–5% |

Meta Platforms (META) | ✅ Yes | ✅ Yes | ~3–4% |

Tesla (TSLA) | ✅ Yes | ✅ Yes | ~2–3% |

Visa (V) | ✅ Yes | ✅ Yes | ~1–2% |

JPMorgan Chase (JPM) | ❌ Excluded | ❌ Excluded | Conventional bank — prohibited both |

Berkshire Hathaway (BRK) | ❌ Excluded | ❌ Excluded | Financial holding company — prohibited both |

Some mid-cap tech/industrial | ❌ Not in S&P 500 | ✅ May be included | HLAL's FTSE universe is broader |

Holdings approximate based on May 2026 data. Exact weights change at quarterly rebalancing. Verify current holdings at spfunds.com (SPUS) and wahedinvest.com (HLAL).

The most important thing in this table: both funds exclude conventional banks entirely. JPMorgan, Bank of America, Wells Fargo, Goldman Sachs — none of them are in either fund. This is the single most significant portfolio difference from a conventional S&P 500 fund.

Performance: Why Both Beat the S&P 500 in 2026

Period | SPUS | HLAL | SPY (S&P 500) | SPUS vs SPY |

|---|---|---|---|---|

Q1 2026 | +8.2% | +7.8% | +7.1% | SPUS +1.1% |

YTD May 2026 | +12.4% | +11.8% | +10.9% | SPUS +1.5% |

2024 Full Year | +24.4% | +23.9% | +23.8% | SPUS +0.6% |

2023 Full Year | +27.8% | +27.1% | +26.3% | SPUS +1.5% |

2022 (Rate hike year) | -20.3% | -21.1% | -18.1% | SPUS -2.2% |

Since SPUS Inception (Dec 2019) | ~+101% | ~+95% | ~+95% | SPUS ahead |

Returns are estimates based on reported fund performance. Past performance does not guarantee future results.

Why Halal ETFs Beat the S&P 500 Most Years

It is not luck. It is the composition. By excluding conventional financial companies (which underperform during stress periods and yield-compression environments) and carrying heavier technology weight (which has led market performance for most of the past decade), Sharia screening has created a structural tilt toward better-performing sectors.

The exception: 2022. Rising interest rates benefited conventional banks — the sector excluded from both halal ETFs. Both SPUS and HLAL underperformed the S&P 500 in 2022 by 2–3 percentage points because they held no banking stocks while banking outperformed. This is the one reliable scenario where halal ETFs lag: rate-hiking cycles that benefit financial stocks.

Over a full market cycle (including both bull markets and downturns), the evidence since 2019 shows halal ETFs matching or slightly exceeding the conventional S&P 500 — while providing better downside protection during financial crises.

Sector Allocation Comparison

Sector | S&P 500 (SPY) | SPUS | HLAL |

|---|---|---|---|

Information Technology | ~29% | ~38% | ~36% |

Healthcare | ~13% | ~15% | ~14% |

Consumer Discretionary | ~11% | ~13% | ~12% |

Industrials | ~9% | ~11% | ~12% |

Financials | ~13% | ~1% | ~2% |

Energy | ~4% | ~4% | ~4% |

Communication Services | ~9% | ~9% | ~8% |

Consumer Staples | ~6% | ~5% | ~6% |

The single most important number in this table: Financials. The S&P 500 has ~13% in conventional financial companies. SPUS has ~1%. HLAL has ~2%. This is the defining structural difference between halal ETFs and conventional index funds — and it is what drives the performance divergence during financial crises.

Liquidity: Why SPUS's Larger Size Matters

SPUS has $892M in assets vs HLAL's $245M. For most individual investors buying $1,000–$50,000 at a time, this difference does not affect your execution. But it does matter in two ways:

Bid-ask spread: SPUS's larger trading volume means the spread between the buy price and sell price is typically tighter — $0.01–$0.02 for SPUS vs $0.03–$0.06 for HLAL. On a $10,000 purchase, this is a $3–$6 difference. Minor, but it compounds if you trade frequently.

Institutional adoption: SPUS's scale makes it more likely to be added to 401k plan menus as an ESG/halal option if you request it from your employer. Larger funds are easier for plan administrators to justify adding.

Where to Buy Both ETFs

Both SPUS and HLAL are available commission-free at every major US brokerage:

Brokerage | SPUS Available? | HLAL Available? | Fractional Shares? |

|---|---|---|---|

Fidelity | ✅ Yes | ✅ Yes | ✅ Yes — buy any dollar amount |

Schwab | ✅ Yes | ✅ Yes | ✅ Yes |

Vanguard | ✅ Yes | ✅ Yes | ✅ Yes (ETF fractional) |

Robinhood | ✅ Yes | ✅ Yes | ✅ Yes — start with $1 |

Wahed Invest | ❌ Not directly | ✅ Yes (primary holding) | Via managed account |

Recommendation: Open your Roth IRA at Fidelity. Buy SPUS as your primary holding with automatic monthly contributions. The combination of zero commission, fractional share availability, and strong IRA interface makes Fidelity the best platform for this strategy.

The Verdict: When to Choose Each

Your Situation | Choose | Why |

|---|---|---|

Building your core halal portfolio, single fund | SPUS | Larger, more liquid, higher historical return, S&P 500 baseline everyone benchmarks against |

Have $10K+ and want two halal ETFs | SPUS (70%) + HLAL (30%) | Methodology diversification; slightly different holdings provide marginal additional diversification |

Prefer the FTSE index methodology | HLAL | Uses total assets denominator (more stable screening); FTSE Shariah index is widely respected |

Want broader exposure beyond S&P 500 large caps | HLAL | FTSE universe includes some mid-cap stocks excluded from the S&P 500 |

Using Wahed Invest managed account | HLAL (automatic) | Wahed primarily uses HLAL in their managed portfolios |

Requesting ETF addition to employer 401k | SPUS | Larger fund size is easier for plan administrators to justify adding |

Frequently Asked Questions

Is SPUS or HLAL better for a Roth IRA?

SPUS is the better core holding for a Roth IRA. The combination of its larger fund size (better liquidity), marginally lower expense ratio (0.49% vs 0.50%), and stronger recent performance record makes it the preferred choice for a long-term, tax-free retirement account. Both are equally Sharia-compliant and both are available commission-free at Fidelity, Schwab, and Vanguard. For investors contributing $500+/month, start with SPUS. Once your halal portfolio exceeds $25,000, consider adding HLAL as a secondary position for methodology diversification.

Does the 0.01% expense ratio difference between SPUS and HLAL matter?

On a $10,000 investment, the difference is $1/year. On $100,000, it is $10/year. The expense ratio difference between SPUS (0.49%) and HLAL (0.50%) is genuinely immaterial for any investment amount a typical retail investor holds. Do not choose between these funds based on a 0.01% fee difference — choose based on the methodology preference and liquidity factors discussed above.

Can I hold both SPUS and HLAL at the same time?

Yes — and for investors with over $25,000 in halal equity ETFs, holding both is a reasonable approach. The 85% holdings overlap means you are not significantly over-concentrating in any single company. The 15% difference creates genuine methodology diversification. A 70/30 or 60/40 SPUS/HLAL split is the most common approach among investors who hold both. Below $25,000, just hold SPUS — the diversification benefit of adding HLAL at smaller portfolio sizes is not worth the complexity.

Are there any other halal ETFs I should consider instead?

For US equity exposure, SPUS and HLAL are the only two options worth considering for a core holding in 2026. Other halal ETFs serve different portfolio roles: AMAL (sukuk — fixed income equivalent), SPRE (Sharia-compliant REITs), and UMMA (actively managed global equity). Build your portfolio with SPUS as the core, then layer in AMAL for stability, SPRE for real estate income, and UMMA for international diversification. HLAL fits as a US equity complement to SPUS, not as a replacement for the other asset classes.

Both SPUS and HLAL are strong, Sharia-compliant, institutional-grade ETFs that have outperformed the conventional S&P 500 since their inception. The choice between them is not about which is "better" in an absolute sense — it is about which methodology preference fits your situation.

For most investors: buy SPUS, hold it in your Roth IRA, and contribute monthly. Add HLAL when your halal equity allocation exceeds $25,000 and you want methodology diversification.

For the complete halal investing guide — including portfolio allocation by age, halal 401k strategies, robo-advisor comparison, and individual stock screening — read our Halal Investing USA 2026 Guide.