You read an article about halal mortgages and encountered musharakah, murabaha, and ijara — all in the same paragraph. You attended a khutbah about riba and realized you understood the prohibition but not how it applies to your 401k. You asked about Islamic investing and someone mentioned gharar and takaful and AAOIFI.

This glossary solves that. Twenty-five essential Islamic finance terms, defined in plain English, with a US-specific example for every single one. Bookmark this page — you will refer to it often.

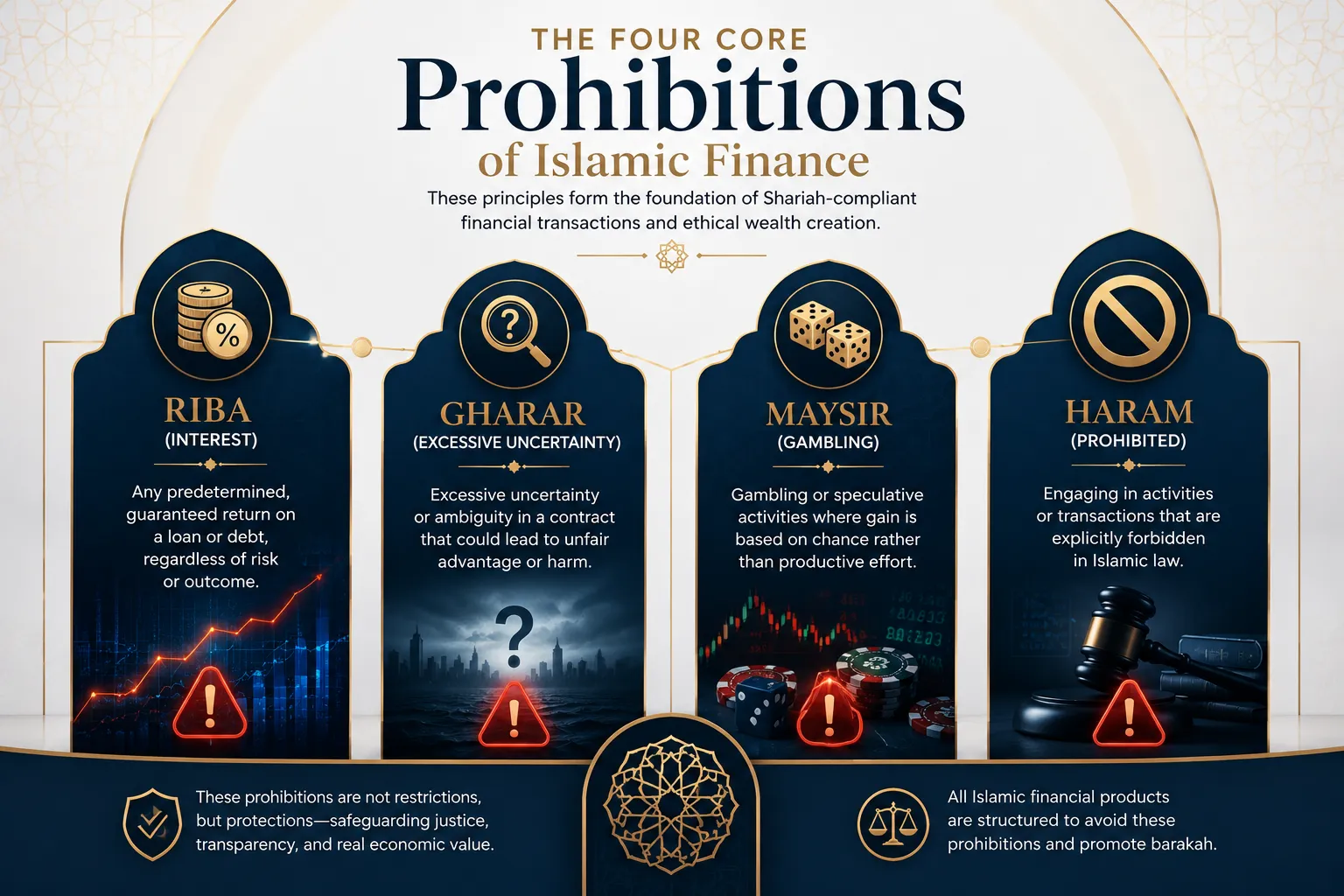

Section 1: The Core Prohibitions

These four terms form the foundation of everything Islamic finance is designed to avoid. Understanding them unlocks why every other term in this glossary exists.

1. Riba (ربا)

What it means: Any predetermined, guaranteed monetary return on a loan based on the passage of time — what the West calls interest. Prohibited in Islamic law because it creates guaranteed profit for the lender regardless of whether the borrower succeeds or fails.

US example: The $430,000 in interest paid on a $400,000 home at a 6.87% conventional 30-year mortgage is riba. So is the 27% APR on a credit card balance, the 5% APY on a high-yield savings account, and the interest component of a target-date 401k fund.

What it means for you: Every Islamic finance product is designed to replace riba with a halal alternative — rent instead of interest on home financing, equity returns instead of interest on savings, profit-sharing instead of interest on business loans.

→ Go deeper: Riba Explained — Complete Guide

2. Gharar (غرر)

What it means: Excessive uncertainty or ambiguity in a contract — particularly when one party holds information that the other does not, or when the subject of the contract is fundamentally unclear. Minor uncertainty is unavoidable and permitted; gharar refers to the kind of uncertainty that makes a contract unjust.

US example: The mortgage-backed securities that caused the 2008 crisis are the classic modern gharar example — investors bought securities rated AAA without knowing the underlying mortgages were subprime. This information asymmetry is exactly what the gharar prohibition addresses. Options, credit default swaps, and most derivatives also involve gharar.

What it means for you: Islamic finance requires that all terms be clear and disclosed. In a halal mortgage, your total cost is disclosed on day one. In a halal investment, you own real equity in real companies — not a synthetic derivative of someone else's position.

3. Maysir (ميسر)

What it means: Gambling or games of chance — gaining wealth through luck rather than productive economic activity. Explicitly prohibited in the Quran (5:90) alongside alcohol.

US example: Casino stocks (MGM Resorts, DraftKings, Caesars Entertainment) are excluded from all halal ETFs and Sharia-screened investment portfolios because their primary business is maysir. Day trading purely for speculative gain also raises maysir concerns among many scholars.

What it means for you: Halal investing screens out all gambling and gaming companies from your portfolio. Returns must come from real productive activity — not from speculation on outcomes disconnected from economic value.

4. Haram (حرام)

What it means: Prohibited under Islamic law. The opposite of halal. In Islamic finance, haram refers to financial activities, industries, and instruments that are forbidden — either because of riba, gharar, maysir, or involvement in prohibited industries.

US example: A conventional 30-year mortgage is haram because it involves riba. JPMorgan Chase stock is haram to hold because the company's primary income is interest. A CD that pays 4.75% interest is haram to keep the returns from (the interest must be donated).

Section 2: Home Financing Terms

If you are researching a halal mortgage, these are the six terms you will encounter in every conversation and document.

5. Musharakah (مشاركة)

What it means: Partnership or joint ownership. In home financing, the bank and you co-purchase the property — you own your down payment percentage, the bank owns the rest. You pay rent on the bank's share while buying it out monthly. As your ownership grows, your monthly payment decreases.

US example: On a $400,000 home with 20% down, you own 20% and Guidance Residential owns 80% from day one. Each month you pay rent on their 80% and buy out a small additional percentage. By year 15, you might own 57%. By year 30, you own 100%. No interest ever changes hands.

What it means for you: You are a co-owner, not a debtor. Your payment decreases over 30 years. If the home loses value, the bank shares the loss proportionally. You save approximately $159,000 vs a conventional mortgage on a $400,000 home.

→ Go deeper: Musharakah Explained — Complete Guide

6. Musharakah Mutanaqisah (مشاركة متناقصة)

What it means: Diminishing co-ownership. The specific form of musharakah used for home financing where the bank's ownership stake is designed from the start to decrease to zero as the buyer buys it out month by month. "Mutanaqisah" means "diminishing" or "decreasing."

US example: Most buyers do not say "musharakah mutanaqisah" — they say "Islamic mortgage" or "halal mortgage." But when Guidance Residential or UIF Corporation describes their home financing product, what they are offering is musharakah mutanaqisah.

7. Murabaha (مرابحة)

What it means: Cost-plus sale. The bank purchases an asset and sells it to you at a disclosed higher price — cost plus profit margin — payable in installments. The total price is fixed at signing and cannot increase. No interest; the bank earns profit through buying and selling, not lending.

US example: Devon Bank purchases your target home for $350,000 and sells it to you for $590,000 (their cost plus their profit margin), payable over 30 years in fixed monthly installments. You agree to this total at signing. It can never become more, regardless of late payments or market changes.

What it means for you: Fixed total cost from day one — complete price certainty. Available nationwide through Devon Bank, making it the accessible option for buyers in states without musharakah providers.

→ Go deeper: Murabaha Explained — Complete Guide

8. Ijara (إجارة)

What it means: Lease or rental. In home financing, the bank purchases the property and leases it to you. You pay monthly rent. You are a tenant, not a co-owner, until the lease ends and ownership transfers via a separate purchase promise.

US example: IjaraCDC purchases your home and leases it to you for 30 years at a fixed monthly payment. At the end of 30 years, you buy the home for $1 under a separate purchase promise. Your payments are level throughout — unlike musharakah's decreasing payments.

What it means for you: Fixed payments, simpler structure, slightly higher total cost than musharakah. Best for buyers who need payment certainty or who live in states without musharakah providers.

→ Go deeper: Ijara Explained — Complete Guide

9. Ijara wa Iqtina (إجارة وإقتناء)

What it means: "Lease ending with ownership." The full name of the lease-to-own structure. Combines an ijara (lease) with a separate wa'd (unilateral promise) that ownership will transfer at term end. The lease and the purchase promise must be two separate documents for the structure to be Sharia-compliant.

US example: When you sign financing documents with IjaraCDC, you sign (1) a lease agreement and (2) a separate purchase option agreement. Both together are "ijara wa iqtina." If they were combined into one document that made purchase a condition of the lease, scholars would reject it as a disguised interest sale.

10. Profit Rate

What it means: The Islamic finance equivalent of an interest rate, used for comparison purposes only. In musharakah, it represents the rental rate applied to the bank's ownership stake. It is not interest — the structural differences in how it is calculated and what it costs over 30 years are significant. Most lenders benchmark it to SOFR (Secured Overnight Financing Rate).

US example: Guidance Residential's profit rate for best-qualified borrowers is 6.74% as of May 2026. The conventional 30-year fixed rate is 6.87%. Despite the lower nominal rate, a conventional mortgage still costs $159,000 more over 30 years because it compounds while the profit rate on a declining balance does not.

What it means for you: Do not compare profit rates to conventional mortgage rates as if they are equivalent. Always compare total 30-year cost using our Halal Mortgage Calculator.

Section 3: Investing and Wealth Terms

11. Sukuk (صكوك)

What it means: Islamic bonds. Unlike conventional bonds (which pay interest), sukuk are backed by real assets and pay a rental yield from ownership of those assets. The sukuk holder owns a proportional share of a real asset (a building, infrastructure project, etc.) and receives the rental income as their return.

US example: The AMAL ETF (Saturna Capital) provides US retail investors access to a diversified portfolio of global sukuk. It yields approximately 4.2% annually — comparable to a conventional bond fund, but through real asset ownership rather than interest. Available at Fidelity, Schwab, and Vanguard.

What it means for you: If you want a fixed-income component in your halal portfolio — for stability, income, or a conservative allocation — sukuk via the AMAL ETF is your primary US option.

12. Halal (حلال)

What it means: Permissible under Islamic law. In Islamic finance, "halal" describes financial products, investments, and transactions that comply with Sharia principles — free from riba, gharar, maysir, and investment in prohibited industries.

US example: SPUS is a halal ETF. An Apple stock position is halal (Apple passes Sharia screening). A Guidance Residential musharakah is halal. A conventional Chase savings account earning interest is not halal for retaining the interest.

13. Sharia-Compliant

What it means: A financial product, institution, or transaction that has been reviewed by qualified Islamic scholars and determined to meet Islamic legal requirements. Not a marketing term — a certifying designation that requires a Sharia board review.

US example: SPUS is Sharia-compliant because Ratings Intelligence Partners (a Sharia advisory firm) reviews and certifies its screening methodology. A company calling itself "Islamic" without a named Sharia board is using the label without the substance.

What it means for you: When evaluating any Islamic finance product, ask: (1) Who is on the Sharia board? (2) Is the fatwa published? (3) Are annual Sharia audits conducted? If a provider can't answer all three, proceed with caution.

14. Purification (Tathir — تطهير)

What it means: The practice of donating the proportion of investment returns attributable to prohibited income. Even halal-screened companies earn small amounts of prohibited income (interest on cash reserves, minor revenue from non-compliant subsidiaries). Purification removes this from your wealth by donating the exact percentage to charity.

US example: SP Funds publishes SPUS's annual purification amount per share. In 2025, it was $0.18 per share. If you held 200 shares, you donate $36 to charity. Zoya calculates purification amounts for individual stocks automatically. This is not optional — it is required alongside Sharia-screened investing.

15. Mudaraba (مضاربة)

What it means: Profit-sharing investment partnership. One party provides capital (the investor), another provides management expertise and labor (the entrepreneur). Profits are split by pre-agreed ratio; capital loss falls on the investor; the entrepreneur's loss is their time and effort.

US example: When you invest in Wahed Invest's managed account, you are effectively entering a mudaraba relationship — you provide the capital, Wahed provides the management expertise. Your return depends on actual investment performance. Wahed earns their fee from managing assets, not from guaranteed interest.

Section 4: Wealth Obligations

16. Zakat (زكاة)

What it means: The third pillar of Islam — a mandatory annual levy of 2.5% on accumulated wealth above a minimum threshold. Unlike income tax (which taxes productivity), zakat taxes accumulated idle wealth, incentivizing capital to remain productive. It is distributed directly to eight specific categories of recipients defined in the Quran (9:60).

US example: If you have $120,000 in net zakatable assets (cash, stocks, 401k net of penalties, gold) above the nisab threshold on your zakat anniversary, you owe $3,000 in zakat (2.5%). Calculate yours with our free Zakat Calculator.

→ Go deeper: Zakat Guide USA

17. Nisab (نصاب)

What it means: The minimum wealth threshold at which zakat becomes obligatory. Defined in weight of gold or silver — not in fixed dollar amounts — so it changes as metal prices change. If your net zakatable wealth is below the nisab, you owe no zakat that year.

US example: As of May 2026, the gold nisab is approximately $9,020 (87.48 grams of gold at ~$3,200/oz). The silver nisab is approximately $634 (612.36 grams at ~$32/oz). Most North American scholars use the gold nisab for modern financial assets.

18. Hawl (حول)

What it means: One complete lunar year (354 days) — the required holding period before zakat becomes due on accumulated wealth. If your wealth exceeds the nisab for a full hawl, zakat is due at the anniversary. If your wealth dips below the nisab during the year, the hawl resets when it rises above again.

US example: If your wealth first exceeded the nisab in Rajab 2025, your first zakat payment is due in Rajab 2026 — not in Ramadan, unless that happens to be your hawl date. Many American Muslims choose to pay during Ramadan (permissible as an early payment) for the increased spiritual reward of that month.

19. Waqf (وقف)

What it means: Islamic endowment — a permanent charitable dedication of an asset. Once declared waqf, an asset cannot be sold, inherited, or given away. Only its income or use goes to the designated charitable purpose. It is the Islamic equivalent of a charitable endowment — like the billion-dollar endowments of Harvard or Oxford, but originating 1,000 years earlier in Islamic civilization.

US example: A mosque in Houston declares its parking lot as waqf for the benefit of Islamic education programs. The mosque cannot sell the parking lot, but the rental income from leasing it to a business funds the school in perpetuity. National Waqf Foundation USA is developing waqf infrastructure for American Muslim communities.

→ Go deeper: Waqf Explained

20. Sadaqah Jariyah (صدقة جارية)

What it means: Perpetual or continuous charity — a charitable act whose reward continues after the giver's death. The Prophet Muhammad (peace be upon him) identified it as one of three deeds that continue after death. Waqf is the institutionalized form of sadaqah jariyah.

US example: Contributing to a mosque's waqf fund, funding an Islamic school's endowment, or donating a well in a water-scarce community are all sadaqah jariyah. A $10,000 waqf contribution invested at 6% annually generates $600/year indefinitely — $60,000 over 100 years — all earning ongoing reward.

Section 5: Governance and Scholarly Terms

21. Sharia Board (هيئة الرقابة الشرعية)

What it means: A committee of qualified Islamic scholars responsible for reviewing, certifying, and monitoring the Sharia compliance of an Islamic financial institution's products. The Sharia board is the mechanism by which "Sharia-compliant" claims are verified — without one, there is no meaningful certification.

US example: Guidance Residential's Sharia board includes Sheikh Yusuf Talal DeLorenzo and other recognized North American Islamic finance scholars. SP Funds' SPUS ETF is certified by Ratings Intelligence Partners. Wahed's HLAL ETF is certified by Amanie Advisors. When evaluating any Islamic finance product, ask for the Sharia board members' names and credentials.

22. AAOIFI

What it means: Accounting and Auditing Organization for Islamic Financial Institutions. The primary international standards body for Islamic finance, based in Bahrain. AAOIFI has published over 100 standards covering Sharia compliance, accounting, and governance for Islamic financial institutions. When a product says it meets "AAOIFI standards," it is following the most widely recognized international framework.

US example: SPUS's screening methodology references AAOIFI Sharia Standard 21 for equity investment screening. The financial ratio thresholds used in halal ETF screening (debt under 33% of assets, interest income under 5% of revenues) come from AAOIFI standards.

23. Fatwa (فتوى)

What it means: A formal scholarly religious opinion issued by a qualified Islamic scholar or body in response to a specific question. In Islamic finance, a fatwa is the document that certifies whether a specific financial product or structure is permissible. Quality fatwas reference specific Islamic legal texts and explain the reasoning — not just the conclusion.

US example: Before Guidance Residential launched its musharakah product, their Sharia board issued a fatwa approving the specific contract structure used. Before SP Funds launched SPUS, Ratings Intelligence Partners issued a fatwa approving the screening methodology. A provider that cannot show you their fatwa (at minimum in summary form) is a red flag.

24. Darurah (ضرورة)

What it means: Necessity — the Islamic legal principle that genuine need can make otherwise prohibited things temporarily permissible. It is the concept scholars apply when a Muslim faces a situation where avoiding the prohibited is genuinely impossible or would cause severe harm.

US example: Most North American Islamic scholars permit American Muslims to use conventional bank checking accounts under darurah — because participating in modern economic life requires a bank account and full-service Islamic banks don't yet exist nationwide. They also permit contributing to an employer 401k under darurah when the match is significant and no halal alternative exists.

What it means for you: Darurah is a legitimate principle — not a loophole for convenience. It applies when you have genuinely exhausted halal alternatives and face real harm from avoidance. It does not apply simply because the halal alternative is slightly more expensive or less convenient.

25. SOFR

What it means: Secured Overnight Financing Rate — the benchmark interest rate published by the Federal Reserve that replaced LIBOR. Most US Islamic mortgage profit rates are benchmarked to SOFR plus a margin. As of May 2026, SOFR sits at approximately 5.30%.

US example: Guidance Residential's 6.74% profit rate for best-qualified borrowers = SOFR (5.30%) + their margin (approximately 1.44%). When the Fed cuts rates, SOFR falls, and Islamic mortgage profit rates typically follow within weeks.

What it means for you: You will see "SOFR" referenced in your halal mortgage documents when the rate is variable. Fixed profit-rate products use SOFR only as a pricing reference at origination — your rate doesn't change afterward.

Quick Reference Table — All 25 Terms

Term | Plain English | Halal or Haram? |

|---|---|---|

Riba | Interest on loans — guaranteed return from time | Haram — the core prohibition |

Gharar | Excessive uncertainty or information asymmetry | Haram — prohibits MBS, derivatives |

Maysir | Gambling or speculation disconnected from value | Haram — prohibits casino stocks, pure speculation |

Haram | Forbidden under Islamic law | Haram by definition |

Halal | Permitted under Islamic law | Halal by definition |

Musharakah | Co-ownership partnership for home or business | Halal — core Islamic finance contract |

Musharakah Mutanaqisah | Diminishing co-ownership — for home financing | Halal — used by Guidance Residential and UIF |

Murabaha | Cost-plus sale — transparent fixed total price | Halal — used by Devon Bank and Lariba |

Ijara | Lease — rent a real asset from its owner | Halal — classical rental contract |

Ijara wa Iqtina | Lease-to-own with separate purchase promise | Halal — used by IjaraCDC |

Profit Rate | Islamic equivalent of an interest rate (for comparison) | Halal — describes rent rate on co-owned assets |

Sukuk | Islamic bonds — backed by real assets, not debt | Halal — AMAL ETF provides US access |

Sharia-Compliant | Reviewed and certified by a Sharia board | Halal designation — verify the board |

Purification (Tathir) | Donating the prohibited income portion of returns | Required practice — not optional |

Mudaraba | Profit-sharing: investor provides capital, manager provides expertise | Halal — used in Islamic investment funds |

Zakat | Mandatory 2.5% annual wealth levy above nisab | Obligatory — one of the Five Pillars |

Nisab | Minimum wealth threshold (~$9,020 gold, May 2026) | Reference threshold — not halal/haram itself |

Hawl | One lunar year — holding period before zakat due | Reference period — not halal/haram itself |

Waqf | Islamic endowment — permanently dedicated charitable asset | Halal and highly encouraged |

Sadaqah Jariyah | Perpetual charity — ongoing reward after death | Halal and highly rewarded |

Sharia Board | Scholars who certify Islamic finance product compliance | Governance mechanism — required for legitimate products |

AAOIFI | International Islamic finance standards body (Bahrain) | Standards reference — look for AAOIFI compliance |

Fatwa | Formal scholarly opinion certifying a product's permissibility | Required for any legitimate Islamic finance product |

Darurah | Necessity — permits prohibited things when genuinely unavoidable | Legal principle — used for conventional bank accounts, 401k |

SOFR | Fed's overnight rate — benchmark for Islamic mortgage pricing | Neutral — pricing reference, not halal/haram itself |

What to Read Next

Now that you have the vocabulary, here is the reading order that builds a complete understanding of Islamic finance for American Muslims:

Riba Explained — Why interest is prohibited and how it appears in modern American finance

Islamic Finance USA 2026 Guide — The complete overview of what is available in the US right now

Halal Mortgage USA — Every provider, current rates, application guide

Halal Investing USA — ETFs, stock screening, 401k strategies

Zakat Guide — Complete zakat calculation for every asset type

Or if you want the fastest path to action: use our Halal Mortgage Calculator to see what an interest-free home purchase would cost for your situation — and our Zakat Calculator to calculate your annual obligation in under 5 minutes.