You have a Chase or Bank of America checking account. You may also have a high-yield savings account earning 4–5% interest. You have heard that riba is one of the most severely prohibited things in Islamic law. Now you are wondering: is having a bank account haram?

The answer is more nuanced than most Islamic finance content admits. Here is what scholars actually say — broken down by account type, with specific named scholarly positions and practical guidance for what to do right now.

The Direct Answer

Having a bank account is not categorically haram. The account itself — as a depository service for keeping your money safe and accessing it through debit cards and transfers — is permissible under the majority scholarly opinion for American Muslims. What is potentially haram is specific to each account type: primarily the interest earned on savings accounts, and, to a lesser degree, the fact that conventional banks use deposits to fund interest-based lending. These are different problems with different solutions.

Breaking It Down by Account Type

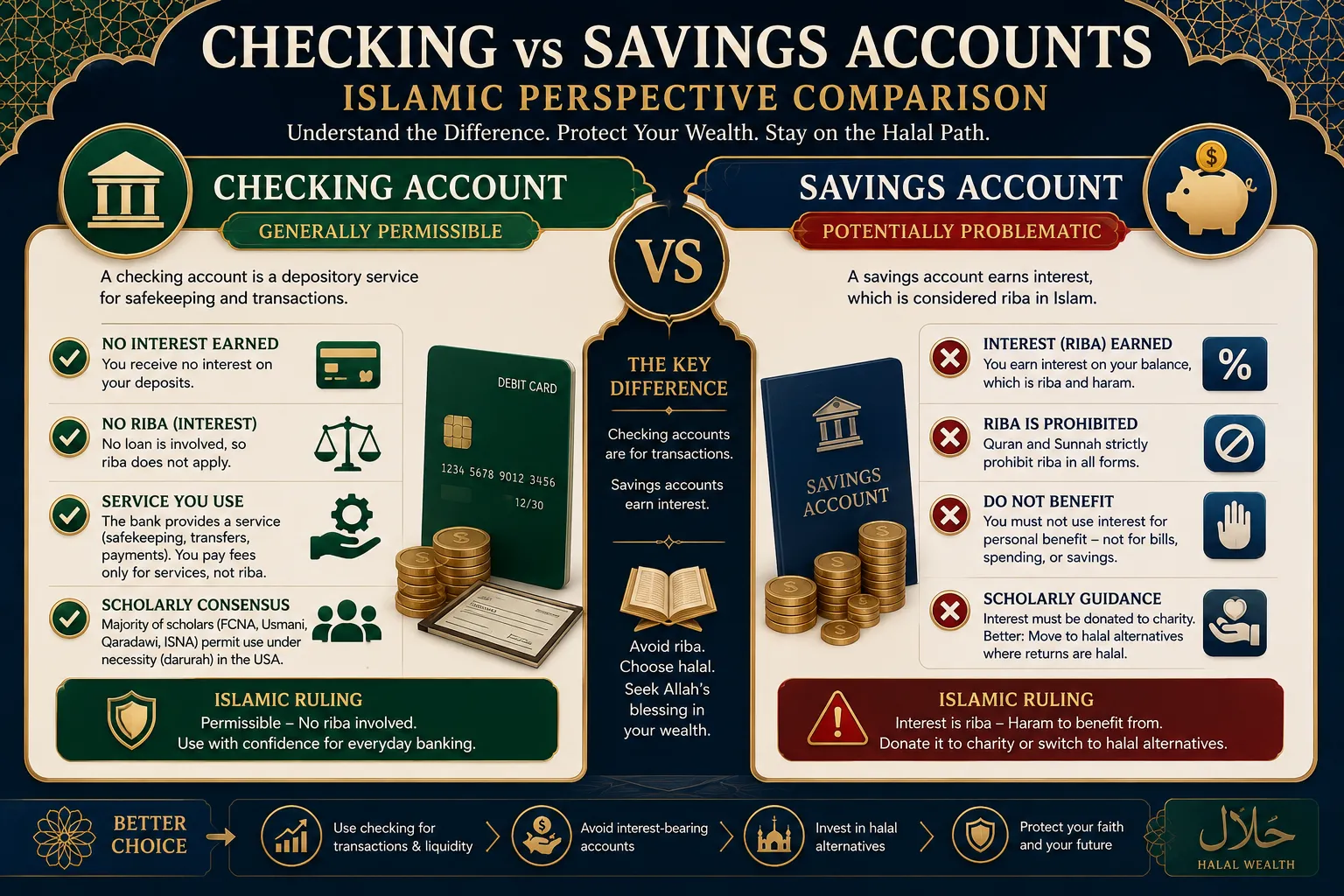

Checking Accounts (Current Accounts) — Generally Permissible

A checking account that earns zero interest is the least problematic form of conventional banking for a Muslim. Here is why most scholars consider it permissible:

It is a depository service, not a financial transaction involving riba. You are using the bank as a custodian for your money — the same function as a safe or a vault — and accessing it through digital tools. The bank provides a service (safekeeping, payment processing, transfers). You pay no interest and receive no interest.

There is no riba in the transaction between you and the bank. Riba requires a loan with predetermined interest. A checking account is not a loan — it is a deposit. The bank owes you your money back on demand; you owe the bank nothing beyond any monthly fees for services rendered.

Darurah (necessity) applies even where some concern exists. In the United States, having a bank account is a practical necessity for modern economic life. Employers require direct deposit. Landlords require bank transfers. Bill payments, online purchases, and everyday commerce require a bank account. Scholars universally recognize that necessity can permit what would otherwise be avoided.

The Fiqh Council of North America — the primary scholarly body issuing Islamic legal rulings for Muslims in North America — has consistently held that using conventional bank current/checking accounts is permissible under the darurah principle, given the absence of widely available Islamic banking alternatives in most US cities.

Savings Accounts and High-Yield Accounts — The Interest Is the Problem

This is where the answer gets more specific — and more actionable. A savings account that earns interest introduces riba into your financial life, but not in the way most people assume.

The account itself is not haram. The structure of a savings account — depositing money, having it available on request — is not inherently prohibited. What is prohibited is keeping the interest.

The distinction matters because it changes what you should do. If the account itself were haram, you would need to close it. Since it is the interest that is problematic, you have a clear path:

Do not spend the interest on yourself — this is the riba that Islamic law prohibits you from benefiting from.

Donate it to charity. This is the scholarly consensus on what to do with interest received from a conventional savings account: purification (tathir). You donate the full interest amount to any charity. You have not benefited from riba; you have removed it from your wealth.

Or: stop earning it in the first place. Move your savings from a conventional HYSA into a halal alternative that generates returns through equity ownership rather than interest. This is cleaner and requires no annual purification calculation.

Money Market Accounts and CDs — Same Analysis as Savings

Money market accounts and certificates of deposit work on the same interest-based mechanism as savings accounts. The same analysis applies: the account structure is not the problem; the interest generated is. Donate the interest or move to halal alternatives. CDs have an additional complexity — you are contractually locked into the interest arrangement for a fixed term. Most scholars advise not entering new CD arrangements and using the maturity date as the exit point.

What About the Bank Lending Your Money for Haram Purposes?

This is the concern some Muslim scholars and community members raise beyond the interest question: when you deposit money in a conventional bank, the bank uses those deposits to fund conventional loans — mortgages, car loans, personal loans, all at interest. Are you complicit in that?

Scholars have addressed this question. The majority position: your deposit does not make you directly liable for how the bank uses pooled funds. The reasoning:

You have not authorized or directed the bank to lend at interest on your behalf.

Your relationship with the bank is a depository service relationship — you are not a partner in the bank's lending operations.

The accountability for the bank's riba-based lending rests on the bank's management and shareholders, not its depositors.

The same darurah principle applies — given the absence of full-service Islamic banks in most US cities, using conventional depository services is a practical necessity.

The more conservative minority position — held by some scholars in the Deobandi tradition — is that Muslims should minimize their support of conventional banking institutions as much as practically possible, even as depositors. This view recommends actively seeking Islamic alternatives and using conventional banks only to the extent genuinely necessary.

Both positions agree on one thing: the obligation to seek Islamic alternatives where they exist and are accessible.

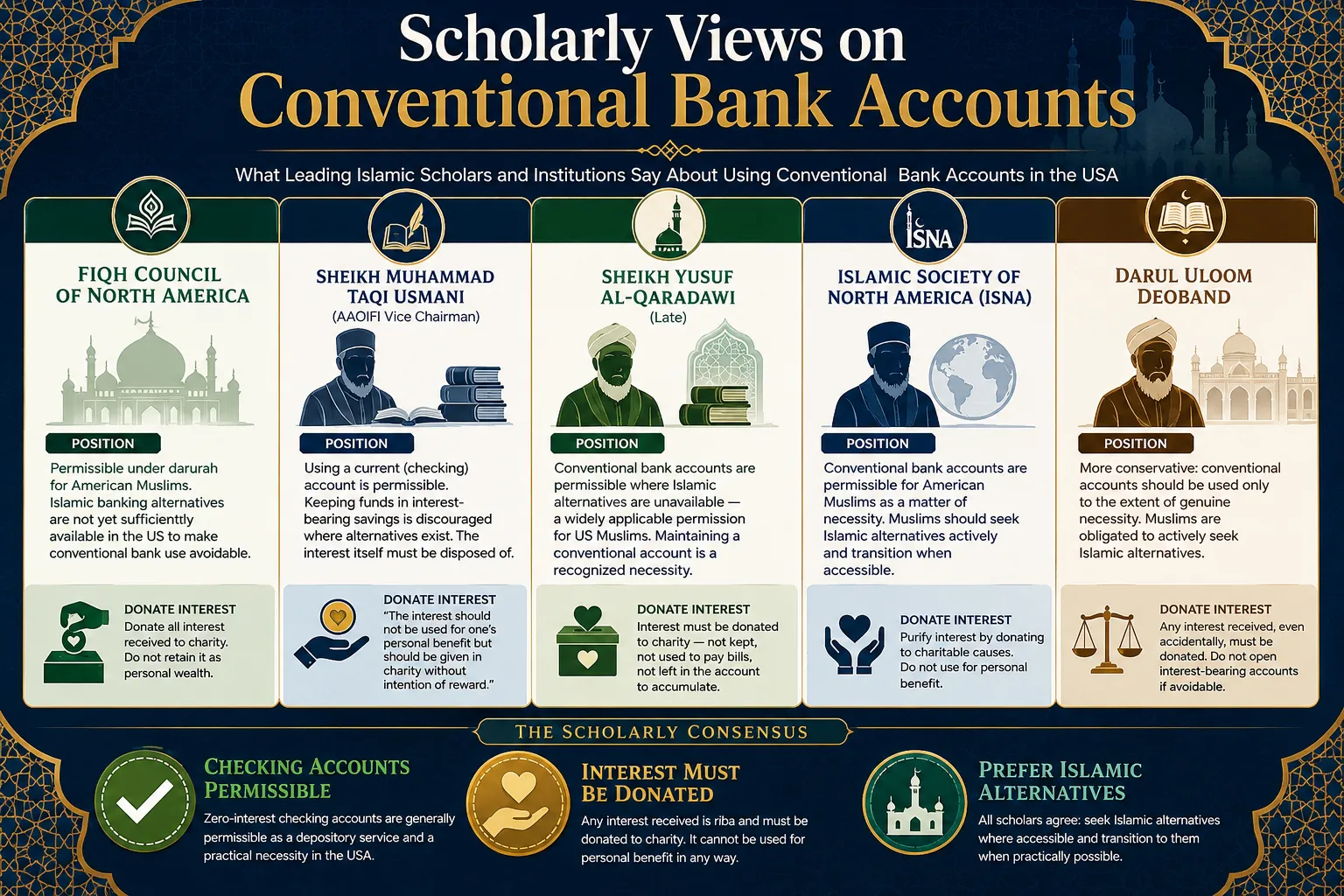

What Specific Scholars Say — Named Positions

Scholar / Authority | Position on Conventional Bank Accounts | What to Do With Interest |

|---|---|---|

Fiqh Council of North America (FCNA) | Permissible under darurah for American Muslims. Islamic banking alternatives are not yet sufficiently available in the US to make conventional bank use avoidable. | Donate all interest received to charity. Do not retain it as personal wealth. |

Sheikh Muhammad Taqi Usmani (Pakistan; AAOIFI vice chairman) | Using a current (checking) account is permissible. Keeping funds in interest-bearing savings is discouraged where alternatives exist. The interest itself must be disposed of. | "The interest should not be used for one's personal benefit but should be given in charity without intention of reward." |

Sheikh Yusuf al-Qaradawi (late; Egypt/Qatar) | Conventional bank accounts are permissible where Islamic alternatives are unavailable — a widely applicable permission for US Muslims. Maintaining a conventional account is not sinful; it is a recognized necessity. | Interest must be donated to charity — not kept, not used to pay bills, not left in the account to accumulate. |

ISNA (Islamic Society of North America) | Conventional bank accounts are permissible for American Muslims as a matter of necessity. Muslims should seek Islamic alternatives actively and transition when accessible. | Purify interest by donating to charitable causes. Do not use for personal benefit. |

Darul Uloom Deoband (traditional South Asian authority) | More conservative: conventional accounts should be used only to the extent of genuine necessity. Muslims are obligated to actively seek Islamic alternatives and should not use conventional accounts out of convenience alone. | Any interest received, even accidentally, must be donated. Do not open interest-bearing accounts if avoidable. |

The consensus across all these positions: The checking account is permissible. The interest from savings accounts must be donated, not kept. US Muslims are obligated to seek Islamic alternatives where accessible, and to transition to them when they become practically available.

What to Do With Interest You Have Already Received

If you have a savings account that has been earning interest — maybe for years — here is exactly what to do:

Calculate the total interest you have received since your last purification (or since you opened the account, if you have never purified). Your bank's statement or the "interest earned" section of your year-end summary gives you this number.

Donate that amount to any charity. There is no requirement that the charity be Islamic. The goal is to remove the riba from your wealth — any legitimate charitable recipient serves this purpose. Many Muslims add this to their annual zakat donation.

Do not count the donated interest as part of your zakat. Zakat is an obligation paid from your permissible wealth. Donating interest for purification is a separate action — it is not charity that earns reward; it is disposal of prohibited income.

Going forward: decide whether to continue purifying annually or switch to halal alternatives.

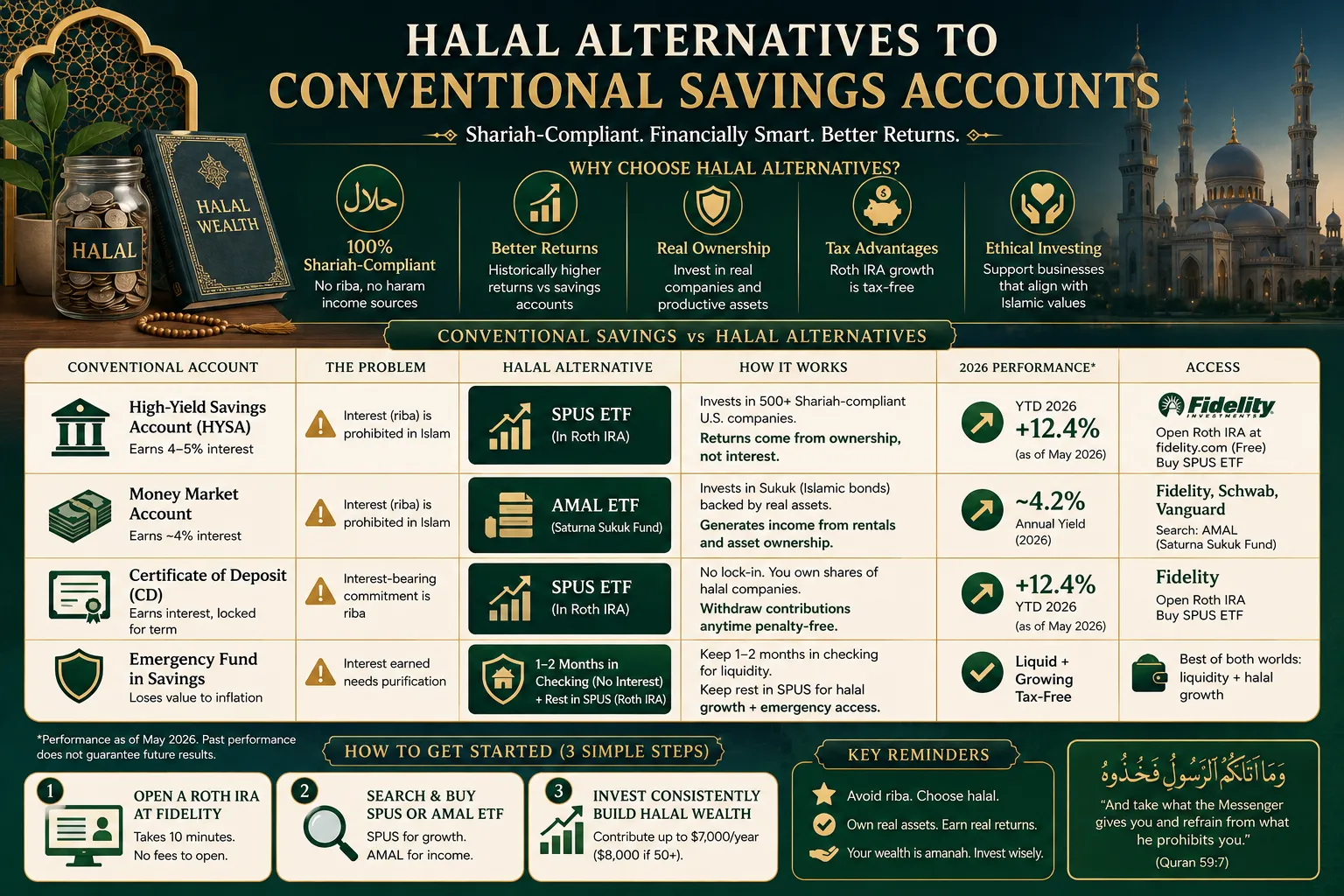

Halal Alternatives to Interest-Bearing Savings Accounts

The most practical halal alternative for most American Muslims is not an Islamic savings account (few exist in the US) — it is investing your savings in halal ETFs through a tax-advantaged account.

Conventional Account | The Problem | Halal Alternative | How to Access |

|---|---|---|---|

Checking account (no interest) | Minimal — primarily the bank's use of deposits | Continue using; no immediate action needed | Stay at your current bank |

High-yield savings account (4–5% interest) | Interest received is riba | Roth IRA at Fidelity invested in SPUS. Returns come from equity ownership, not interest. YTD 2026: +12.4% (vs HYSA ~4.5%) | Open at fidelity.com (free, 10 minutes); buy SPUS; contribute up to $7,000/year |

Money market account | Interest income is riba | AMAL ETF (Saturna sukuk fund) for stable, lower-volatility returns from real asset rental income, not interest. ~4.2% annual yield | Available at Fidelity, Schwab, Vanguard |

Certificate of deposit (CD) | Interest-bearing, locked-term riba commitment | Do not renew. At maturity, move to SPUS in Roth IRA or AMAL for income-oriented needs | Plan exit at maturity date |

Emergency fund in savings | If interest-bearing: needs purification | Keep 1–2 months in checking (no interest). Rest in SPUS in Roth IRA (Roth contributions can be withdrawn anytime penalty-free) | Roth IRA contribution withdrawal rules apply |

What About the Emergency Fund?

The conventional advice is to keep 3–6 months of expenses in a liquid savings account. The halal approach:

Keep 1–2 months in a zero-interest checking account. Truly liquid, no riba concern, available instantly.

Keep the remaining 2–4 months in a Roth IRA invested in SPUS. Roth IRA contributions (not earnings) can be withdrawn at any time, for any reason, with no taxes and no penalty. This gives you emergency access while your money earns halal equity returns rather than riba.

This restructuring — checking account for liquidity, Roth IRA for medium-term emergency reserves — is how many financially sophisticated American Muslims structure their cash management to minimize riba exposure practically.

Islamic Banking Options in the US (Limited But Growing)

For Muslims who want a full-service Islamic banking relationship rather than using conventional banks at all, options are limited in the US but growing:

University Bank / UIF (Ann Arbor, Michigan) — offers some Mudarabah-structured savings products alongside their mortgage business. Most accessible in Michigan.

Saturna Capital — Islamic checking and savings accounts alongside their Amana Fund investment products. Available nationwide.

Some credit unions in Michigan, Texas, and California have developed Sharia-compliant deposit products for Muslim community members. Check with your local mosque community for recommendations.

The reality for most American Muslims in 2026: a full-service Islamic bank equivalent to a conventional Chase or Bank of America — with branches, full digital services, and FDIC insurance — does not yet exist nationwide. This is why the darurah permission for conventional accounts remains practically relevant for most US Muslims.

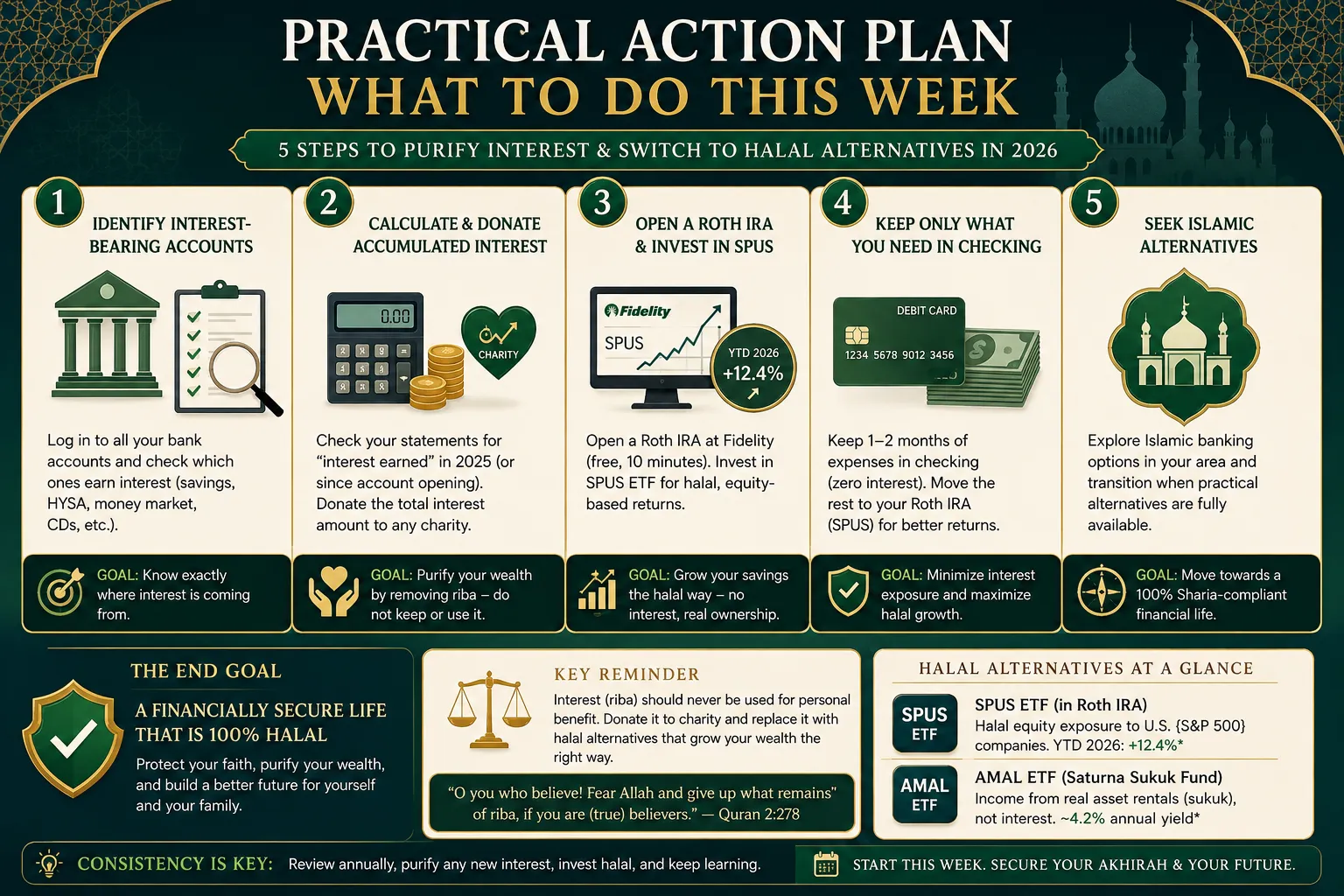

The Practical Action Plan — What to Do This Week

Identify which of your accounts earn interest. Log into every bank account and check whether it pays any interest rate. Zero-interest checking accounts require no immediate action. Interest-earning accounts need the purification step.

Calculate and donate accumulated interest. Check your year-end bank statement for total interest earned in 2025. Donate that amount to any charity before your next zakat calculation date. Use our Zakat Calculator to handle both zakat and purification in one calculation.

Open a Roth IRA at Fidelity and buy SPUS. This is the single most impactful action for most American Muslims. Your savings earn returns through equity ownership rather than interest. Maximum contribution: $7,000/year (under 50) or $8,000 (age 50+).

Keep only what you need for monthly expenses in checking. The less money sitting in interest-bearing accounts, the less interest accumulates that requires purification.

Frequently Asked Questions

Is it haram to have a bank account in Islam?

No — having a bank account is not categorically haram. The majority scholarly position, including the Fiqh Council of North America and Sheikh Muhammad Taqi Usmani, permits using conventional bank accounts for American Muslims as a recognized necessity (darurah). A zero-interest checking account raises minimal Sharia concern. A savings account that earns interest requires donating the interest to charity (purification) rather than keeping it.

Is bank interest haram even if I didn't choose it?

Yes — interest received is riba regardless of whether you actively sought it. If your bank automatically credits interest to your savings account, that interest is riba. The appropriate response is not to keep it as your wealth. Donate it to charity to remove it from your financial life. The sin of riba lies in benefiting from it — not in the mechanical fact that a bank credited it to your account.

Can I use interest I received to pay bills?

No — this is the specific prohibited use. Using interest income for your own personal benefit — including paying bills, buying food, or any other personal expense — is retaining riba as part of your wealth. The required action is to donate the full interest amount to charity. You cannot use it yourself in any form, even for a "good" purpose like paying off debt. Donate it, separately, to a charitable cause.

Is PayPal, Venmo, or Cash App haram?

Payment apps that simply transfer money between accounts are not inherently haram — they are payment processing tools, not financial products that generate interest. If a payment app offers a "balance" feature that earns interest (PayPal and some others do), the same analysis applies as a savings account: the app itself is not haram, but the interest earned should be donated. Turn off interest-earning balance features if your payment app offers them.

Should I close my savings account and put everything in a Roth IRA?

For most American Muslims, yes — this is the most practical restructuring available right now. A Roth IRA at Fidelity invested in SPUS gives you: halal returns from equity ownership (not interest), tax-free growth, and the ability to withdraw your contributions penalty-free at any time for genuine emergencies. The SPUS YTD return of +12.4% through May 2026 compared to a savings account's 4.5% APY makes the halal alternative financially superior as well as Sharia-aligned. Contribution limits apply ($7,000/year under 50).

The answer to "is it haram to have a bank account" is not a simple yes or no. It is: the checking account is fine; the interest on your savings account needs to be donated; and there are practical halal alternatives for your savings that are both Sharia-compliant and currently outperforming interest-bearing accounts anyway.

For the complete guide to halal investing as a replacement for interest-bearing savings, read our Halal Investing USA 2026 Guide. For retirement account strategies — including what to do about 401k interest exposure — read the Halal Retirement Planning guide.