Texas is one of the best states in America to buy a home using halal financing — not because of any special state law, but because the combination of a large and concentrated Muslim population, strong provider competition, and relatively affordable home prices (outside Austin) makes the numbers work better here than almost anywhere else in the country.

This guide covers every halal mortgage provider serving Texas, current profit rates as of May 2026, a city-by-city breakdown for Houston, Dallas, Austin, and San Antonio, and the exact application process for a Texas buyer.

Halal Mortgage Options in Texas — May 2026

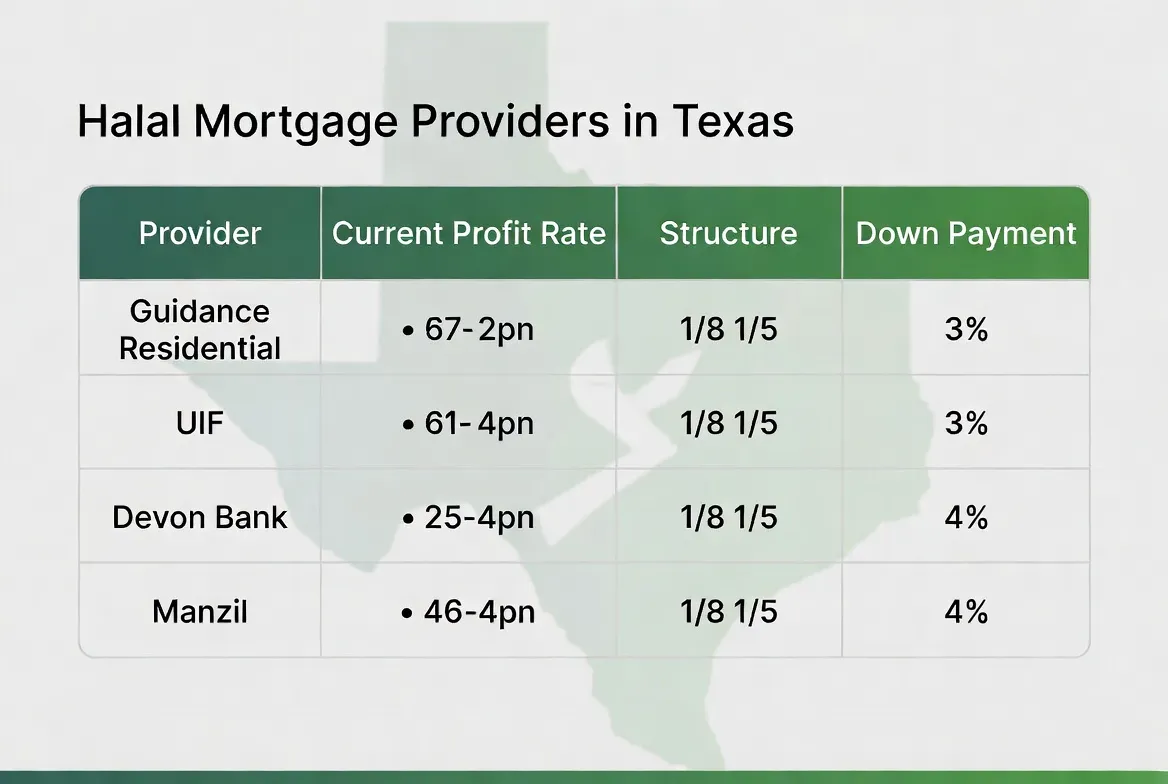

Four Islamic home financing providers actively serve Texas as of May 2026. Here are their current rates and key details for Texas buyers:

Provider | Structure | Best Rate (720+ FICO) | Standard Rate (680 FICO) | Min Down | Texas Cities Served |

|---|---|---|---|---|---|

Guidance Residential | Musharakah | 6.74% | 7.12% | 5% | Statewide — all major metros |

UIF Corporation | Musharakah | 6.89% | 7.24% | 20% | Statewide — strong in Houston |

Devon Bank | Murabaha / Ijara | 7.10% | 7.45% | 20% | Nationwide — all Texas |

Manzil | Musharakah | 7.25% | 7.55% | 20% | Dallas/Fort Worth primary focus |

Rates as of May 2026. Profit rates vary by loan amount, down payment, credit profile, and property type. Contact providers for personalized quotes.

For most Texas buyers, Guidance Residential is the starting point — lowest rates, widest product range, and the only provider offering below 20% down payment options. If you are self-employed or need more flexible income documentation, add UIF Corporation to your comparison. Use our Halal Mortgage Calculator to model your payments at current Texas rates.

What Halal Mortgages Actually Cost in Texas — Real Numbers

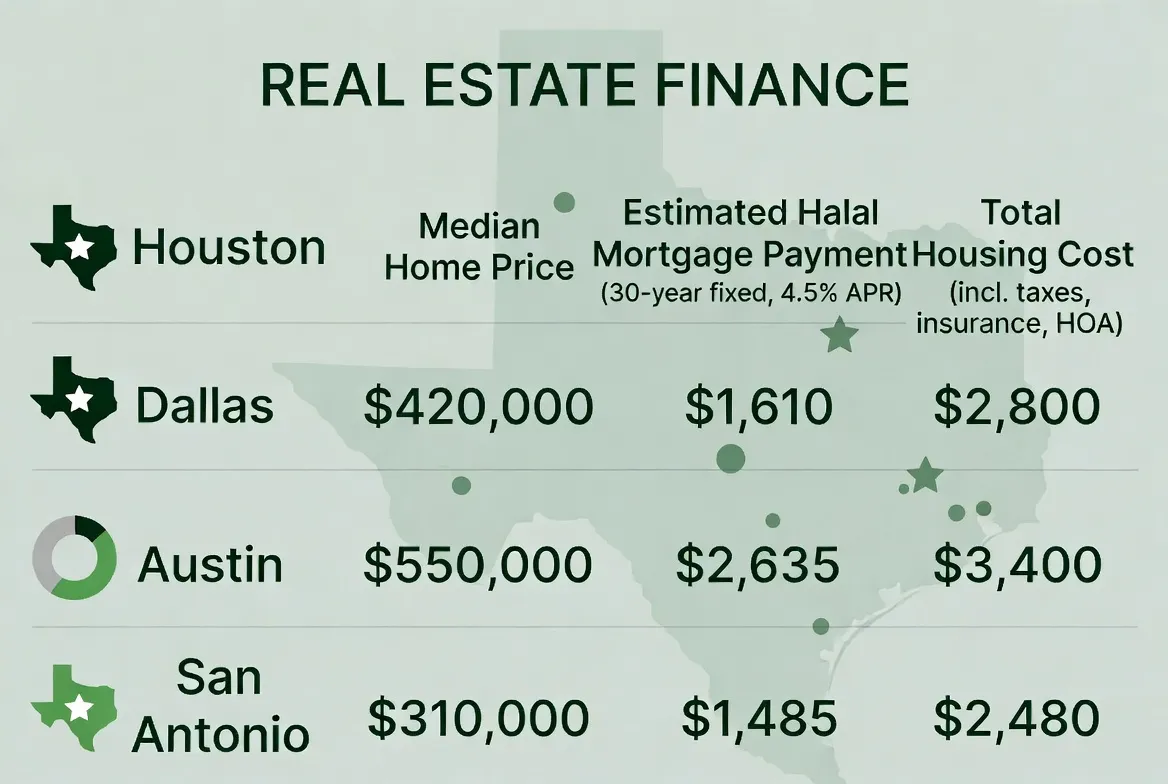

Texas property taxes are higher than the national average — typically 1.5–2.5% of assessed value annually, depending on county. This matters when calculating total monthly housing costs. Here is what a halal mortgage looks like in each major Texas market at May 2026 rates, with property taxes included:

City | Median Home Price | 20% Down | Finance Amount | Monthly Payment (7%) | Est. Property Tax/Mo | Total Monthly Cost |

|---|---|---|---|---|---|---|

Houston | $270,000 | $54,000 | $216,000 | $1,860 (Month 1) | ~$430 | ~$2,290 |

Dallas/Fort Worth | $340,000 | $68,000 | $272,000 | $2,340 (Month 1) | ~$570 | ~$2,910 |

San Antonio | $250,000 | $50,000 | $200,000 | $1,722 (Month 1) | ~$380 | ~$2,100 |

Austin | $480,000 | $96,000 | $384,000 | $3,305 (Month 1) | ~$900 | ~$4,205 |

Payment shown is Month 1 at 7.0% profit rate — musharakah payments decrease each month. Property tax estimates based on county averages: Harris County ~1.9%, Tarrant/Dallas County ~2.0%, Bexar County ~1.8%, Travis County ~2.2%. Texas has no state income tax — factor this into your overall affordability assessment.

City-by-City Halal Mortgage Guide

Houston — The Strongest Texas Market for Halal Financing

Greater Houston has approximately 100,000 Muslim residents — the largest Muslim community in Texas — concentrated primarily in the Southwest Houston corridor: Sugar Land, Missouri City, Stafford, Katy, and the Meyerland neighborhood. All four halal mortgage providers serve the Houston metro.

Houston's median home price of $270,000 is among the most affordable major-metro markets in the country for the income levels of the Muslim professional community. At 20% down ($54,000), the finance amount is $216,000 — well within qualifying range for households earning $80,000+.

Houston-specific tip: Sugar Land and Missouri City have the highest concentration of title companies and real estate agents familiar with Islamic mortgage documentation in Texas. When your real estate agent asks about your financing type, specifying "Musharakah co-ownership" rather than "Islamic mortgage" tends to produce faster recognition from experienced agents in these areas.

Dallas / Fort Worth — A Rapidly Growing Market

The Dallas/Fort Worth Metroplex has approximately 90,000 Muslim residents, concentrated in Plano, Irving, Richardson, Garland, and Carrollton. The DFW market has seen significant home price appreciation — median prices in Plano and Frisco now exceed $500,000 — making the down payment requirement the primary challenge for many buyers.

Guidance Residential's 5% down payment option is particularly relevant in DFW, where home prices are higher. At 5% down on a $380,000 home, the down payment is $19,000 vs $76,000 at 20% — a significant accessibility difference for buyers still building savings.

DFW-specific tip: Tarrant County and Dallas County both have property tax rates around 2.0–2.2%. Always run your affordability calculation including property tax — in DFW, property tax can add $700–$900/month to your housing cost, which meaningfully affects your debt-to-income ratio for qualification purposes.

San Antonio — The Most Affordable Texas Option

San Antonio has a smaller but growing Muslim community (~20,000 residents) and the lowest median home prices of any major Texas city at approximately $250,000. The combination of lower prices, the musharakah structure's decreasing payment benefit, and Texas's no-income-tax environment makes San Antonio the most financially accessible market in Texas for halal homebuyers.

Guidance Residential and Devon Bank both serve San Antonio. UIF Corporation also covers the San Antonio metro. Given the smaller Islamic finance origination volume in San Antonio compared to Houston or DFW, processing times may run slightly longer — budget 55–65 days rather than 45–55.

Austin — Higher Prices, Strong Provider Coverage

Austin has experienced the most dramatic home price appreciation of any Texas city — medians reached $550,000+ at the 2022 peak before settling to approximately $480,000 in 2026. The Muslim community is smaller (~25,000) but growing rapidly as tech industry employment draws Muslim professionals from across the country.

At Austin's prices, the 20% down payment requirement is a real barrier: $96,000 on a median-priced home. For Austin buyers, Guidance Residential's 5% down program is the most important variable — $24,000 down on a $480,000 home vs $96,000 is the difference between buying now and waiting several more years to save.

Austin-specific tip: Travis County has some of the highest property tax rates in Texas (~2.2%). On a $480,000 home, annual property taxes can reach $10,500+ — approximately $875/month. Include this in your monthly budget calculation before applying.

Texas-Specific Legal Considerations

Texas has unique property laws that affect Islamic mortgage structuring in ways that buyers should understand:

Texas Homestead Law

The Texas Constitution provides exceptionally strong homestead protections. Under Article XVI, Section 50, a homeowner's primary residence (homestead) is protected from forced sale for most debts. For musharakah co-ownership structures, Texas title companies document the co-ownership agreement in a way that preserves homestead protection for the buyer's ownership share. All major providers (Guidance, UIF) have established Texas-compliant documentation for this.

No State Income Tax

Texas has no state income tax. This is financially significant for halal mortgage buyers because it increases take-home income available for down payment savings and monthly payments. A household earning $120,000 in Texas pays $0 in state income tax vs approximately $4,000–$7,000 in states like California or New York. This free cash flow accelerates down payment accumulation — directly addressing the primary access barrier to halal mortgages.

Texas Property Transfer Process

Texas uses a deed of trust system (not a mortgage lien system used in some other states). Musharakah co-ownership in Texas is typically structured through a grantor trust or a tenancy-in-common arrangement with a co-ownership agreement — both of which are fully recognized under Texas property law. Texas title companies in Houston and DFW are increasingly familiar with Islamic mortgage documentation; smaller markets may require your lender to provide additional guidance to the title company.

Step-by-Step: Buying a Home in Texas Without Interest

Run your Texas-specific numbers (10 minutes). Use our Halal Mortgage Calculator with your target city's median price. Add the estimated property tax for your target county (1.8–2.2% annually) to understand your total monthly housing cost. Texas property taxes are paid through an escrow account with your monthly payment — your lender will include this in the total payment figure.

Contact Guidance Residential first (15 minutes). Call or apply online for pre-qualification. For Texas buyers with W-2 income and 720+ credit, Guidance offers the best available rates. Ask specifically about the 5% down program if you have less than 20% saved.

Add UIF if you are self-employed. If you own a business or have non-W-2 income, get a parallel pre-qualification from UIF Corporation. Their bank statement income program accepts 12–24 months of business deposits as income documentation.

Choose your Texas real estate agent carefully. In Houston, DFW, and Austin, there are real estate agents with specific experience managing Islamic mortgage closings. Ask your lender's loan officer for agent referrals in your target market — they work with these agents regularly and can connect you.

Lock your rate once under contract. Texas's competitive real estate markets in DFW and Austin can move quickly. Once you are under contract on a property, lock your profit rate immediately — rates can move in a week following Fed announcements.

Budget 50–60 days to close. Inform your seller and real estate agent that your closing timeline is 50–60 days. In competitive offer situations, this is slightly longer than conventional — a brief explanation to sellers ("co-ownership Islamic mortgage — federally approved, same process but one additional documentation step") reduces friction significantly.

Frequently Asked Questions — Texas Halal Mortgages

Is there a halal mortgage in Houston?

Yes. All four major US halal mortgage providers serve Houston: Guidance Residential, UIF Corporation, Devon Bank, and Manzil. Houston has the largest Muslim population in Texas (~100,000) and the strongest Islamic finance market in the state. Southwest Houston — Sugar Land, Missouri City, Stafford, and Katy — has the highest concentration of Muslim homebuyers and the most title company experience with Islamic mortgage documentation.

Is there a halal mortgage in Dallas or Fort Worth?

Yes. Guidance Residential, UIF Corporation, Devon Bank, and Manzil all serve the Dallas/Fort Worth metro. The Muslim community is concentrated in Plano, Irving, Richardson, Carrollton, and Garland. DFW's higher median prices ($340,000–$500,000+ in Plano/Frisco) make Guidance's 5% down option particularly relevant for first-time buyers.

Do I need to be Muslim to get a halal mortgage in Texas?

No — any Texas resident can apply for a halal mortgage regardless of religion. Approximately 20–23% of Islamic mortgage customers in the US are non-Muslim. Providers do not require religious identification, and Texas anti-discrimination law prohibits any such requirement. The products are available to everyone.

How do Texas property taxes affect my halal mortgage payment?

Texas property taxes (1.5–2.5% annually depending on county) are collected through an escrow account with your monthly payment — exactly like conventional mortgages. Your lender divides your annual property tax obligation by 12 and adds it to your monthly payment. On a $300,000 home in Harris County (Houston), this adds approximately $450–$475/month to your payment. Always include property taxes in your affordability calculation — they are a material component of total housing cost in Texas.

Can I use a halal mortgage for a new construction home in Texas?

Yes. New construction homes are eligible for musharakah and Ijara financing with all Texas providers, subject to the property passing standard appraisal. The key consideration: construction loans (financing the building process before the home is complete) have a different structure from standard purchase financing. For new construction, confirm with your lender whether they finance construction completion or only the purchase upon completion. Most Texas Islamic mortgage providers finance the purchase of completed new construction — not the construction phase itself.

Texas Muslim homebuyers have better Islamic financing options today than at any point in history — four active providers, competitive rates, and a housing market where the numbers work outside of Austin. The down payment is the primary barrier for most buyers. If you are building toward it, Texas's no-income-tax environment gives you more take-home income to save faster than almost any other state.

Use our Halal Mortgage Calculator to see your exact monthly payment at current Texas rates — enter your city's median price or your specific target home value.

For the complete halal mortgage guide covering all structures, all providers, and the full application process, read our Halal Mortgage USA 2026 Guide. To see all verified Islamic finance providers in your specific Texas county, visit our Texas Local Options page.